The Roundtable Hold of EU Trades - Greens With a Side of Thermal

Browsing the trade opportunities offered by a continent that focused on the side quest - starting with what the energy situation implies.

We regulate minutiae—like plastic bottle caps shaped to reduce litter (and yes, probably the shape of cucumbers, too)—yet beneath this meticulous policymaking, we juggle a trio of major headaches: a war in Ukraine that shattered illusions of perpetual peace, a likely Trump 2.0 with an allergy to trade deficits (bad news for the EU’s prized exports), and an energy debacle that has factories and households paying record-high bills. As if that weren’t enough, we’re also determined to push green energy agendas, insisting we can decarbonize and keep the lights on economically—despite shuttering nuclear reactors and passionately embracing wind and solar. Welcome to modern Europe, where illusions of sovereignty crumble around what feels like a continent-sized museum.

Figuring Out What European Sovereignty Means

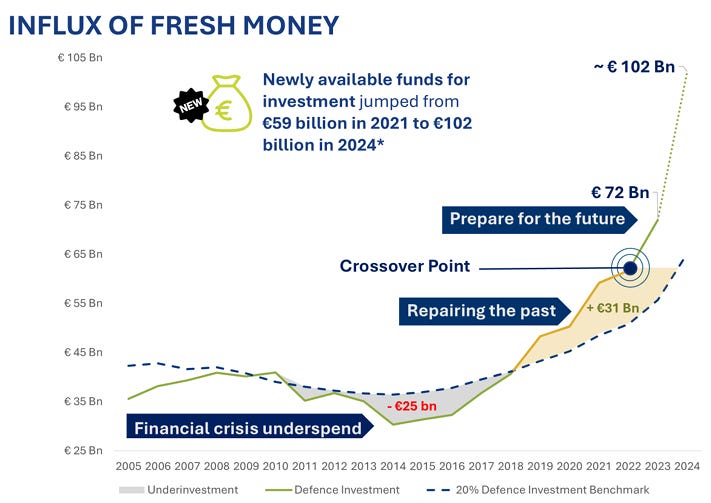

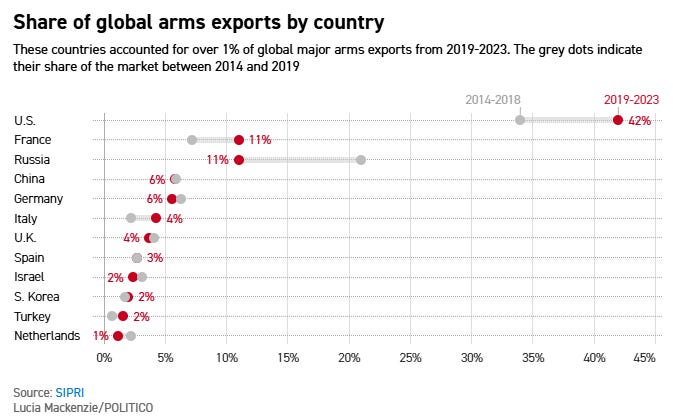

For decades, we assumed the Cold War’s end let us shift budgets from tanks to social good. France, Germany, Italy—all savored the “peace dividend,” kindly underwritten by the leader of the free world. Then 2022 arrived, bringing Russian forces shelling Ukrainian cities. Suddenly, Europe realized it needed an actual army, not just parades. Germany launched a special €100 billion fund to fix its famously under-equipped Bundeswehr. Poland jumped to spending 4% of GDP on defense. Ministers clamored for artillery shells, drones, advanced jets. Investors, in turn, showered European arms makers—like Rheinmetall and BAE Systems—with capital, doubling or tripling their share prices in under two years.

Yet behind triumphant announcements about new tank orders lies an awkward truth: modern defense production devours energy. Steel mills for tank hulls, chemical plants for explosives, aluminum smelters for aircraft frames—these processes are exceptionally power-hungry. If your kilowatt-hour price is two- or three-times the global average, courtesy of costly imported gas, you’re building a “strategic” army on a very wobbly economic footing. Meanwhile, the White House might slam 25% tariffs on your biggest exports unless you sign a contract for F-35s. There’s the tension: do we plow new defense euros into American gear so they spare BMW or Hermès from tariffs, or attempt a purely European defense buildout, even if our electricity costs are sky-high?

Why Trump 2.0 Will Likely Target Europe

Washington has already shown it’s willing to tariff neighbors like Canada and Mexico—close allies who basically have to follow along. Europe, in contrast, can be a messy friend, often squabbling about digital taxes, climate policies, or ignoring U.S. pleas to buy more U.S. jets. For an administration that sees trade deficits as an insult, Europe’s large surplus (especially in autos, luxury, chemicals) is a sitting duck. It’s not hard to imagine a White House ultimatum: “Buy my missiles, or I’ll slap 25% on your cars and handbags.” For smaller EU states specialized in a single export niche, that’s disastrous. For bigger ones like Germany, losing the U.S. car market can complicate the next election. In a flourish, officials might accept large Lockheed Martin or Raytheon deals to appease Washington—despite loud claims of wanting a pan-European defense project.

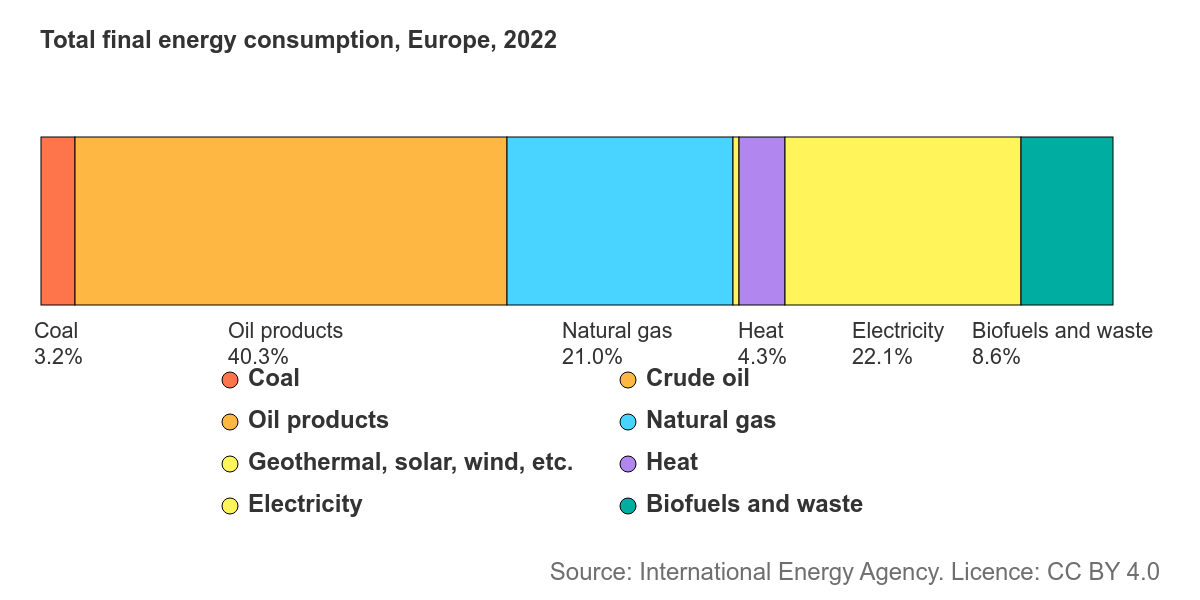

But consider our deeper problem: an overdependence on foreign energy that, by 2022, covered over 62.5% of our total consumption. Historically, we had cheap Russian gas while we wrote “green transition” laws, closing domestic coal mines and nuclear plants faster than new renewables could fill the gap. Then the Ukraine invasion cut off that pipeline flow, sending prices five- to tenfold higher. So just as the White House could brandish tariffs, we can’t easily retaliate by banning American LNG. We rely on it now! If a new Trump standoff emerges, it’s the U.S. that holds the bigger leverage—thanks to our lingering energy vulnerability.

Still, there’s a silver lining for Europe’s broader markets: if U.S. data continues to show ~150k jobs added per month, stable productivity, and subdued inflation, the overall risk environment often favors both equities and bonds simultaneously. Historically, that has led to strong inflows into under-owned European stocks and government debt, especially from countries like France or Italy that have a mild “credit” component.

(starting to form a deflationary impulse case for the U.S. which I will dig into more after we get the next CPI and PPI prints)

2022 Energy Crisis is Still Here Today

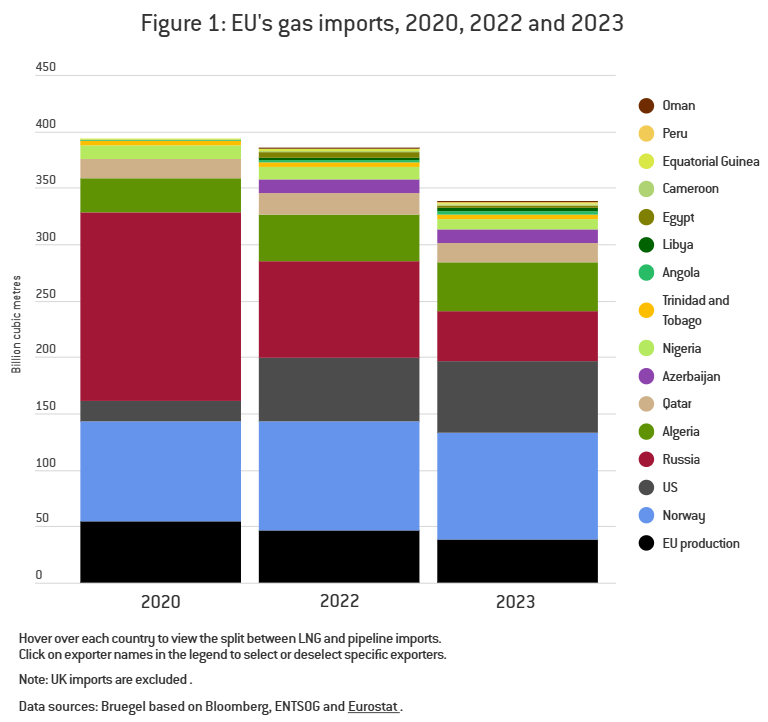

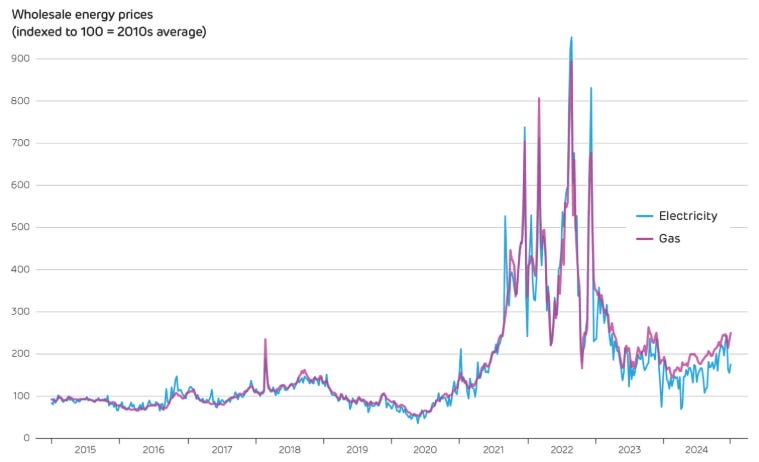

In the blink of an eye, Europe’s “energy sovereignty” mantra went from polite dinner talk to a screaming siren. For years, we told ourselves that scaling wind and solar—plus some Russian gas as a “bridge”—would suffice. Then that “bridge” became a weapon for Moscow in 2022. We learned we couldn’t pivot to renewables overnight: reaching 50% or more of the grid with intermittent power demands robust storage, backups, and strong interconnectors. Meanwhile, Germany and others had already closed nuclear plants, phased out local coal under climate pledges, and cut gas production in the Netherlands. So when the crisis hit, we lacked fallback options. TTF gas soared above €300/MWh, metals and fertilizer plants shut, and governments spent hundreds of billions on subsidies.

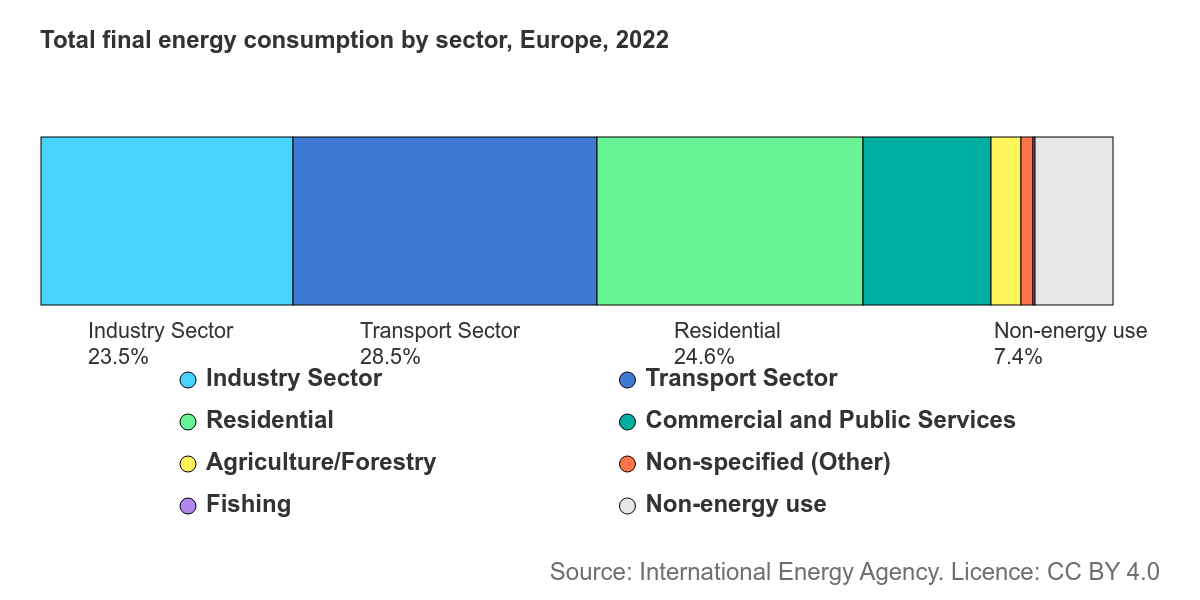

Wind and solar power compensated for about one-third of the shortfall, coal and gas plants covered another 10%, but using scarce gas to produce electricity meant we still had to cut electricity demand by around 5%. Now that we pivoted to LNG from the U.S. and Qatar, we’re somewhat more diversified but remain heavily import-dependent. Even if peace arrives in Ukraine tomorrow, returning to cheap Russian supplies is politically unlikely. That suggests we’ll keep paying higher prices for alternative sources, hoping renewables ramp up fast enough to stabilize costs. The deeper paradox: we champion a green transition, but until we solve intermittency and baseload generation, we’re tethered to fossil imports—especially from new suppliers like the U.S. That’s an uneasy place to be if Washington starts threatening duties in other areas.

Europe’s Green Side Quest vs Reality

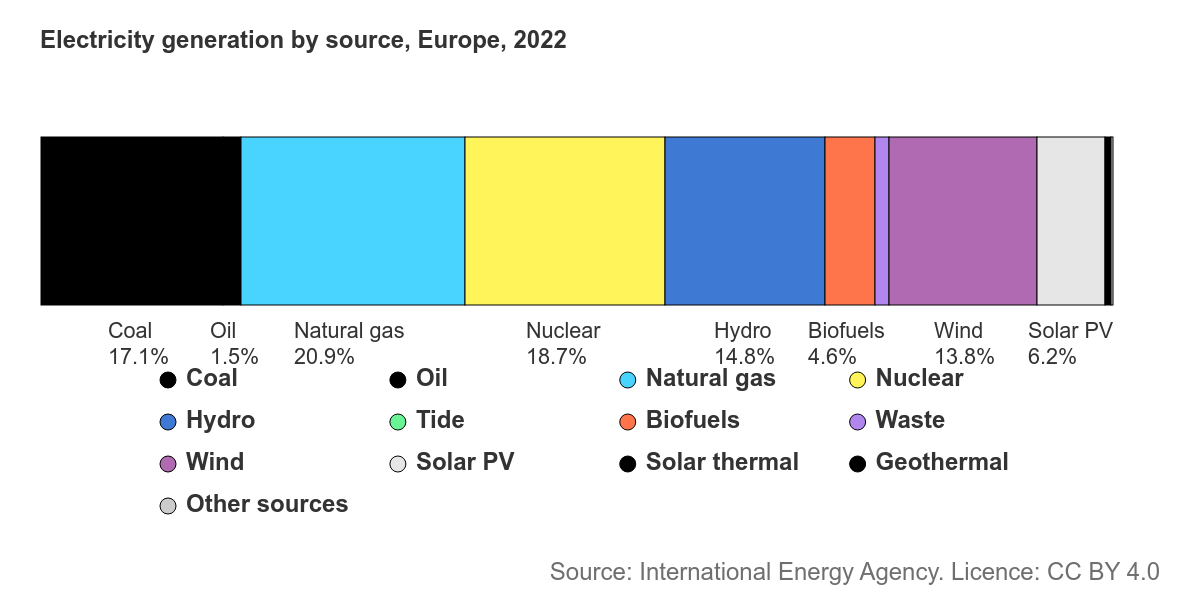

It’s not that our green ambitions lack merit. We’ve built a robust framework for decarbonization, from emissions trading to the European Green Deal, boosting renewables to 41% of EU electricity in 2022. By 2030, we aim for at least 42.5% of total energy from renewables. That, in principle, reduces reliance on imported fossil fuels. But the transition so far has been disorderly: some states closed local gas fields (for environmental reasons) faster than new technologies arrived, meaning in 2021–22 we still needed massive Russian gas to keep German factories running. Then we lost that pipeline supply and discovered our wind turbines can’t fill gaps during calm weather—prompting a coal usage spike or greater LNG imports.

We have limited gas storage, minimal battery capacity, and a smattering of cross-border interconnections. Whenever a big lull in wind occurs—like the infamous German Dunkelflaute—we resort to gas or coal, draining reserves just when we need them most. Our local fossil production keeps shrinking, and although we add solar and wind aggressively, we still rely on global fossil markets. That’s not exactly robust “sovereignty.” For now, energy prices will continue at a premium in Europe.

Even so, from a market perspective, Europe’s under-owned, lower-valuation profile can still draw capital—particularly when global growth is “not too hot, not too cold” and inflation hovers near central bank targets. In past cycles (like early 2019), that dynamic led to strong risk-adjusted returns for European stocks.

When the Wind Don’t Blow and the Sun Don’t Shine…

Against this fraught backdrop, two nations stand at a crossroads, epitomizing Europe’s tangled energy future. Germany, the self-styled renewable champion, is suddenly exposed by the very revolution it heralded. Meanwhile, Norway—long hailed for its clean hydropower—continues to derive significant prosperity from oil and gas, leaving it tethered to the old-energy world.

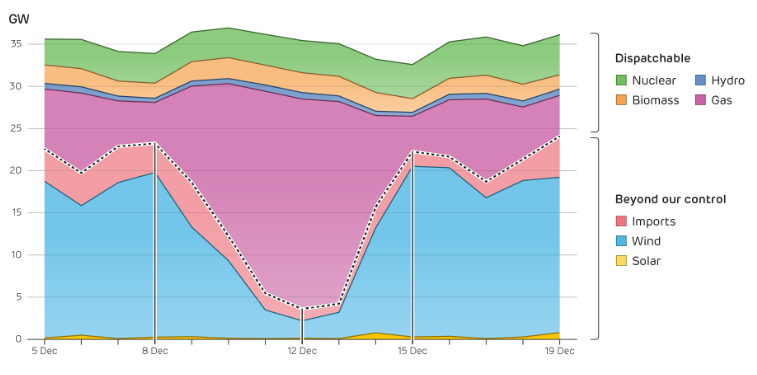

Germany’s Energiewende was seen as a beacon, supposedly guiding the planet toward a wind-and-sun-powered utopia. But the winter Dunkelflaute of 2025 unmasked painful vulnerabilities: renewable generation plunged to 5 GW on February 5—far below the levels of December 2023—compelling coal, dismissed as a relic, back online at 8.1 GW (its highest usage since early 2024). Because Germany is integral to Europe’s interconnected grid, any shortfall there sends shockwaves throughout the region. When Berlin must import electricity, neighbors like the UK and France see prices spike, exposing just how dependent everyone remains on stable baseload. Natural gas still props up the rest, yet it’s hardly the pristine solution once pitched.

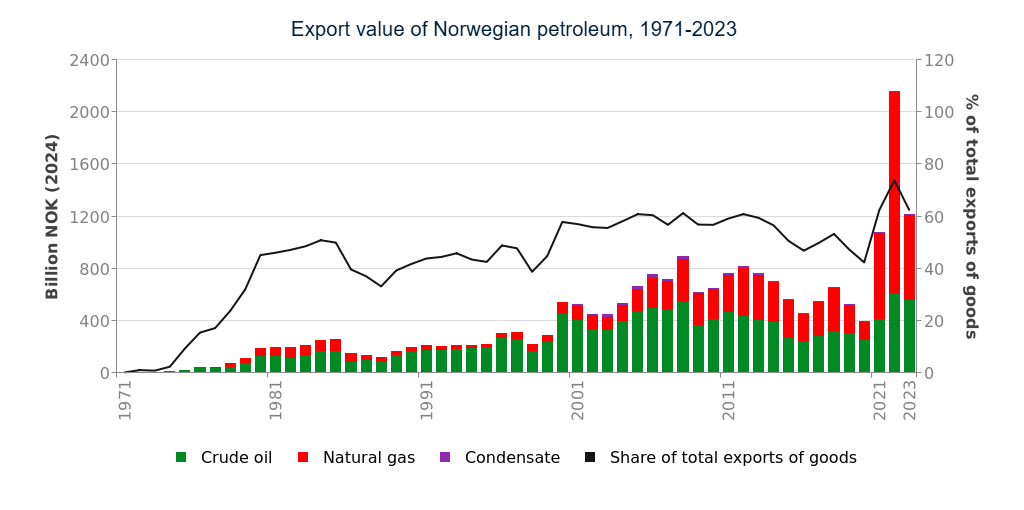

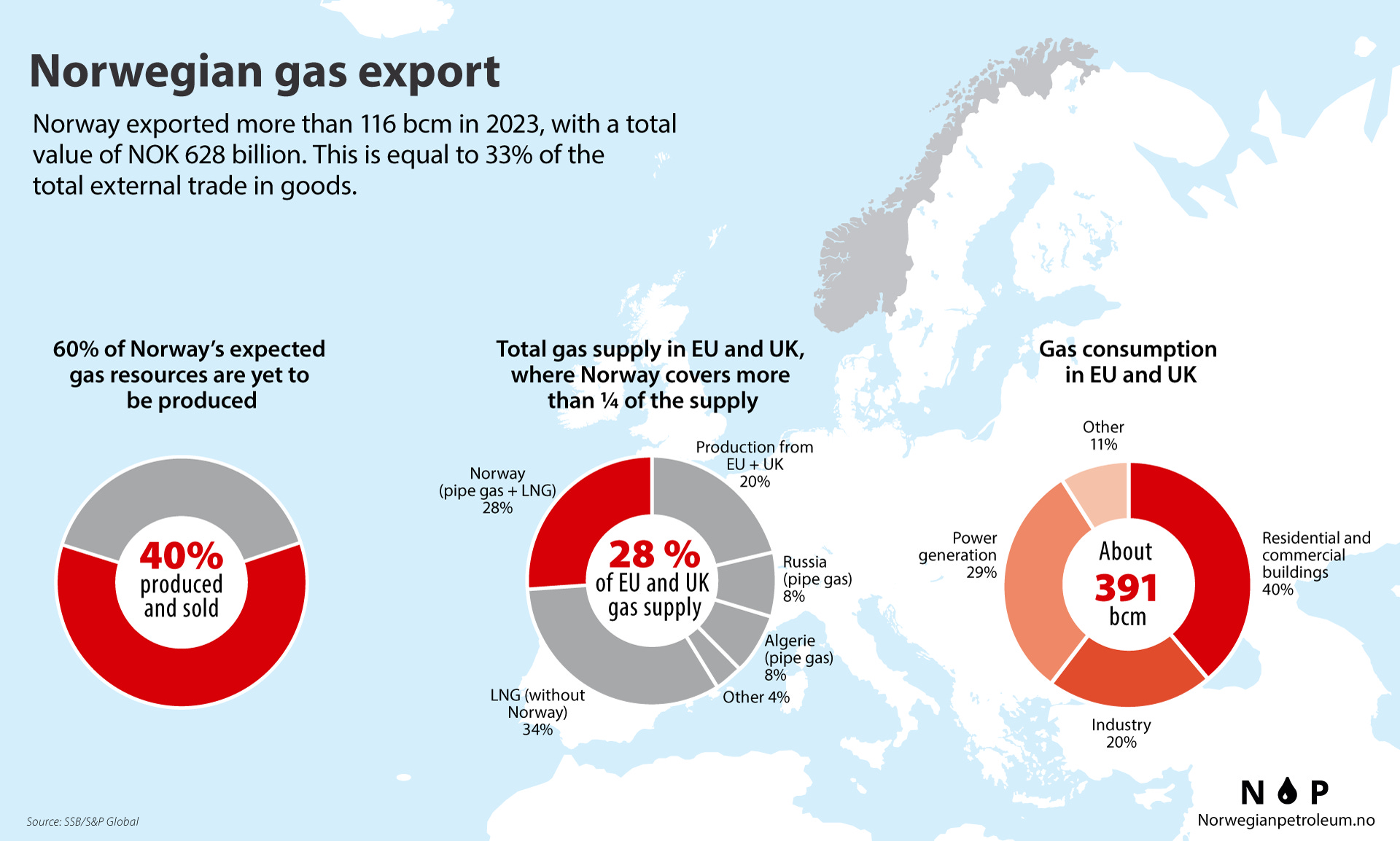

Amid Germany’s coal resurgence, Norway emerges as Europe’s reluctant savior. Harnessing hydropower for 90–95% of its electricity, Norway plugged the gap again in 2024 by exporting 9 TWh to the UK and 14 TWh to Germany whenever German renewables fell short. But this altruism strains domestic reserves. Norwegian electricity prices rose 35% year-on-year, fueling public outcry over “exporting away” cheap power. The Centre Party withdrew support for Oslo’s energy policy, while Prime Minister Jonas Gahr Støre proposed price freezes to placate voters. Underlying it all, Norway depends on oil and gas for about 15% of its GDP. A sudden slump in global gas demand could jolt Norway’s economy, while an EU energy meltdown might intensify calls to clamp down on exports—potentially fracturing Europe’s fragile unity.

Paradoxically, Norway is also pushing the decarbonization envelope in offshore oil and gas. By electrifying fields like Sleipner, cutting 300,000+ tonnes of CO₂ annually, and pioneering the Hywind Tampen floating wind farm (which powers oil platforms with renewable electricity), Oslo pulls off the neat trick of burning fewer hydrocarbons to produce hydrocarbons. Battery-powered supply vessels reduce offshore emissions further. Yet behind this green veneer, Norway’s wealth hinges on fossil exports. Even “bridge fuel” natural gas might fall from grace if Europe’s climate fervor accelerates, raising profound questions about Norway’s long-term energy identity. Every TWh diverted abroad drives up local utility bills, triggering political backlash and tarnishing Norway’s once-unassailable reputation as an eco-paragon.

Germany’s quick pivot to coal, meanwhile, underscores the precariousness of leaning heavily on intermittent renewables without robust backups. Norway’s simmering domestic tension spotlights how being Europe’s “green battery” comes at a steep political cost. Ultimately, this tug-of-war reveals a sobering fact: transitioning from fossil fuels is infinitely more complicated than glossy policy brochures suggest. If solidarity frays—perhaps Norway caps exports to safeguard its own citizens, or Germany doubles down on coal for grid security—Europe’s dream of a seamless renewable future faces mounting challenges. These two nations stand on the front line of a puzzle the entire continent must resolve: how do we reconcile lofty climate ambitions with the unyielding demands of energy security?

New Defense Spend, Old Energy Fault Lines

So, can we truly rearm while saddled with high energy costs? If steel, aluminum, or chemicals are battered by gas bills, producing artillery or advanced drones becomes pricier. Some states—like France, with 70% nuclear electricity—are less exposed to gas shocks. But many rely on gas-fired power, and a White House ultimatum might coerce smaller EU nations into buying American arms just to dodge new tariffs. It’s hardly the ideal blueprint for a cohesive European defense industry, already fragmented by local job protection and procurement feuds.

EU policymakers now scramble to fix these glaring gaps: more strategic gas reserves, new LNG terminals in Germany built in record time (they had none before), and a possible partial nuclear revival in once-nuclear-shy states. The Ukraine war accelerated all of this. But it doesn’t magically lower near-term power bills. Our domestic fossil output keeps shrinking; renewables, though scaling quickly, can’t cover the full shortfall anytime soon. We remain net importers for ~63% of our total energy—limiting our scope to retaliate if the U.S. brandishes tariffs. They know it, we know it—so guess who holds the stronger hand?

Even so, if global investors continue to see decent productivity gains in the U.S. and moderate inflation readings, risk appetite can support both European credit and sovereign bonds. In prior periods of stable 1.5–2% growth and ~2% inflation, bonds from countries like Italy and France delivered strong, predictable returns—a trend that might repeat if energy worries subside.

Could a Peace in Ukraine Spark a Mean Reversion?

One might hope a Ukraine ceasefire helps global energy prices dip, removing the “war premium” and letting battered European equities rebound. Historically, the end of conflict in Europe can deliver a “peace dividend,” lifting cyclical sectors, restoring business confidence, and nudging the ECB to friendlier rate stances if inflation cools. That scenario would see BASF or steelmakers reactivating capacity, consumer shares rallying, and maybe the euro strengthening as war risk fades.

But we likely won’t revert to cheap Russian pipeline deals. Politics and trust are shattered—especially in Eastern Europe. So the best we get is partial relief: enough for cyclical names to bounce off lows, but not enough to fix structural supply gaps. Our precarious green transition lurches on, with short-term reliance on LNG at steep prices. Still, in a “goldilocks” global setting—steady U.S. job growth, mild inflation, modest global GDP—European equities historically flourish. A partial Ukraine peace could amplify that rally by easing energy jitters.

Greens With a Side of Thermal

One might assume Europe’s policy chaos is cosmic punishment. But for markets, these swirling tensions aren’t just comedic fodder: they produce investment opportunities. Our scramble to square the circle—go green but still burn coal, protect trade while risking tariffs, build up defense while energy costs soar—creates winners and losers. Below are the near-term trades that could thrive as the Old Continent wrestles with modern crises.

A Barbell Philosophy: Rebound Plays vs. Energy-Secure Winners

Underneath these specific trades, there’s a unifying strategy: two-speed Europe. On the one hand, companies in energy-reliant countries (like Germany, Italy, Czechia) got pummeled by the 2022 crisis and could rebound strongly if energy normalizes. On the other, energy-secure economies (France, Iberia, Norway) and their flagship firms may continue chugging along—or even flourish—thanks to stable domestic resources or structural policy support.

How It Works:

Rebound Potential in Hard-Hit Industrials

Think of chemical and manufacturing giants like BASF (Germany) or steelmakers like ArcelorMittal (with major EU exposure). If gas prices keep easing and costly imports fade, battered margins could jump back. The risk is that some capacity has permanently moved overseas, but a decent stretch of stable gas would still give these firms a hefty upswing off depressed share prices.Steady Gains for Energy-Secure Markets

Meanwhile, Norway’s Equinor or Spain’s Iberdrola enjoy robust domestic supply or diverse renewables. Even if Europe’s gas troubles flare up again, they remain comparatively shielded—and might even capitalize on the next scramble for non-Russian supply. This half of the barbell provides a hedge if cyclical, high-energy industries fail to bounce.

Use this dual approach as a guiding principle across the trades outlined below. It helps reconcile the tension between short-term cyclical rebounds (in hammered industries) and long-term structural advantages (in resource-rich or renewables-savvy economies).

Coal Producers: The Zombie Industry

(Potential Winners: Glencore (GLEN.L), Peabody Energy (BTU), RWE (RWE.DE), Whitehaven (WHC.AX), Yancoal (YAL.AX), Thungela (TGA.L)) - Not my favored area but a small allocation might be warranted

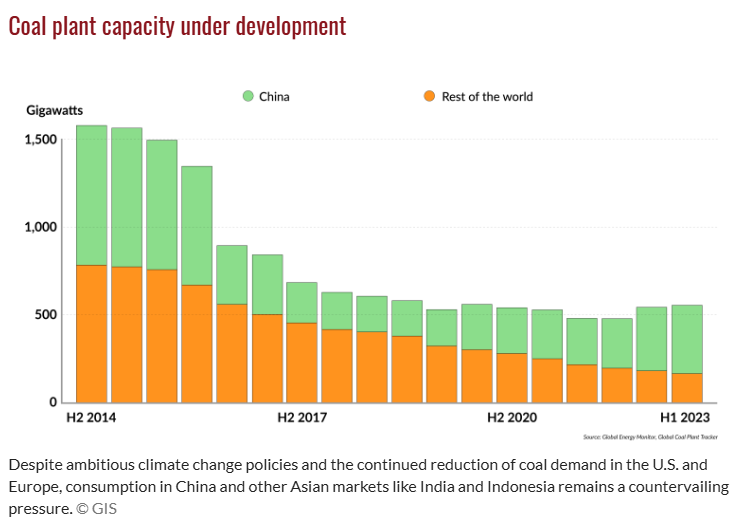

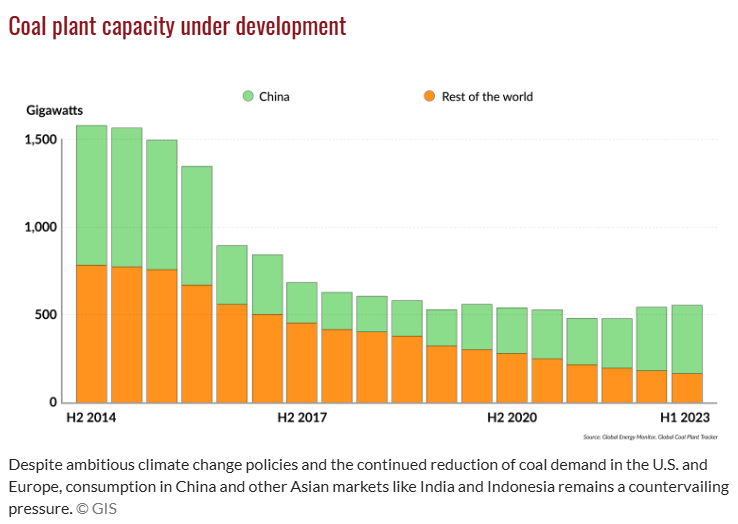

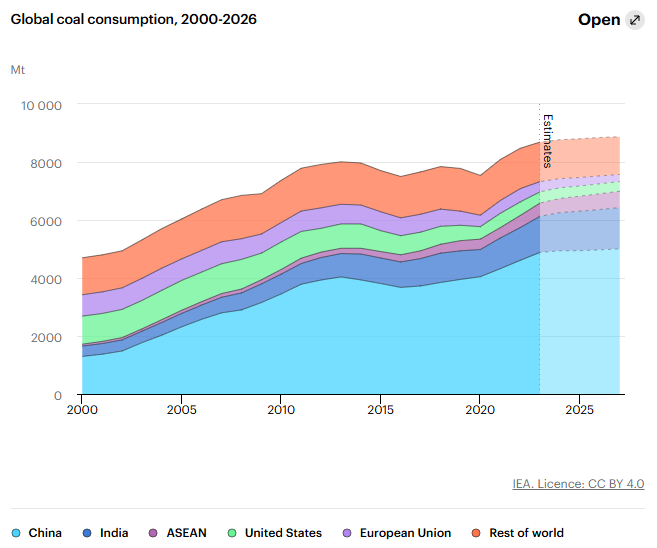

It’s a paradox for the ages: the more the EU talks up net-zero ambitions, the more it resorts to extending or restarting coal-fired plants whenever Russian gas falters or the wind refuses to blow. Glencore and Peabody Energy saw record profits thanks to Europe’s scramble in 2022–23, while RWE continues to rely on its “dirty” coal fleet to balance renewable capacity. The short-term story is clear: nobody wants to admit Europe still needs coal, yet that’s exactly what keeps happening each winter.

Why They Benefit

Fallback Hero When Gas Is Costly

As long as gas prices remain elevated—and renewables remain intermittent—coal serves as the unwanted-yet-essential Plan C. Countries like Germany may announce coal phaseouts, but those targets often slide once cold winters or energy shortfalls loom.Asia’s Demand Outweighs Europe’s Decline

Europe gets the headlines for phasing out coal, but the real growth engine is Asia. China and India, in particular, continue building new coal plants to meet surging electricity demand. Even if Europe slightly curbs its usage, Asia’s expansions more than offset those reductions. This keeps the seaborne coal market tight and price-supportive.

Chronic Underinvestment Keeps Supply Tight

Investor pressure, ESG mandates, and a widespread narrative of “coal is doomed” have starved the sector of capital. That ironically sustains higher prices: few new mines, minimal exploration, and cautious producers mean global supply can’t ramp quickly when demand spikes. The result? Coal remains a reliable cash generator for those who still produce it.Thermal and Met Coal Both in the Picture

While thermal coal (power generation) grabs the spotlight, metallurgical (coking) coal for steel is equally crucial. Cities keep rising, infrastructure expands, and steel remains indispensable in emerging markets. Many coal companies (e.g., Peabody, Whitehaven) tap both thermal and met markets, enjoying a more diversified earnings base.The Zombie Resource

Coal is the zombie of energy generation, the tomb-stone has been planted but its still slowly walking around. Even as Europe claims the moral high ground by trimming usage, global seaborne markets remain firm. Combine that with cost inflation and production constraints, and coal often becomes the reluctant fallback whenever anything else fails. No matter how disliked, it’s still there in the corner—thriving on necessity.

Risks to Keep in Mind

Regulatory Crackdowns & Sin Taxes

Coal is the easiest political target in the EU, so watch for sudden taxes, forced early closures, or strict emissions penalties that could hammer profits. Australia’s Queensland royalty hike shows how local governments can swoop in on windfall earnings.Reputational & ESG Pressures

Even if fundamentals are bullish, reputational risk can depress valuations. Many funds simply refuse to hold coal, shrinking the pool of potential buyers—though the flip side is that low valuations can present outsized return potential for those willing to stomach the stigma.Demand Shocks or Policy Swings

A synchronized global recession could momentarily cut power demand and steel consumption, denting coal prices. Meanwhile, any big breakthrough in renewables-plus-storage—or a genuine nuclear renaissance—could reduce coal’s fallback role over time.

LNG Majors: Ride the Transatlantic Gas Express

(Potential Winners: Equinor (EQNR), Shell (SHEL), TotalEnergies (TTE), Cheniere Energy (LNG) - plenty more dyor) - Higher conviction here than Coal

Why They Benefit

Europe’s Gas Lifeline: The Pivot to LNG

Russia’s invasion of Ukraine shattered Europe’s energy assumptions. Almost overnight, pipeline gas from Moscow—once the backbone of Europe’s energy system—was no longer an option. Desperate to keep the lights on and factories running, European governments turned to liquefied natural gas (LNG)—a market previously dominated by Asian buyers.

U.S. exporters like Cheniere and global trading houses like Shell and TotalEnergies found themselves in the trade of a lifetime. With Europe scrambling for supply, LNG prices soared, and sellers dictated the terms. Norwegian energy giant Equinor, traditionally a pipeline supplier, also saw its influence grow, stepping in as Europe’s new “reliable gas champion” amid the chaos.

The Reality: Europe Still Needs LNG

Even as the immediate crisis subsides, Europe’s dependency on LNG isn’t going away anytime soon. Governments are spending billions on regasification terminals, betting that Russian pipeline gas is a thing of the past. And while renewables are ramping up, they’re not yet reliable enough to replace the role gas plays in heating, industry, and power generation.

For companies like Cheniere, this means locked-in demand for years to come. LNG exporters with existing infrastructure—especially those with operational terminals—are in a sweet spot: Europe can’t afford to wait for new projects to come online, so it’s stuck paying a premium for existing supply.

Limited U.S. Shale Expansion Keeps the Market Tight

Investors hoping for a surge in U.S. shale gas production to flood the LNG market may be in for a disappointment. Top-tier shale fields are maturing, and supermajors are favoring share buybacks over aggressive drilling. That means the pipeline of new LNG projects remains constrained—good news for incumbents like Cheniere and Equinor, who will continue to command strong margins.

The LNG Majors Are Locking in the Future

Knowing that today’s tight market won’t last forever, LNG giants are locking in long-term contracts at highly favorable rates. The Qataris, who boast the world’s lowest-cost LNG, are aggressively expanding, but most of their new supply won’t be online until later this decade. In the meantime, Shell and TotalEnergies are securing multi-decade deals with Asian and European buyers, ensuring steady cash flows even if spot prices fall.

Risks

What if Russian Gas Makes a Comeback?

If Europe finds itself warming up to Russian pipeline gas once again, even in limited amounts, other sources of LNG imports could fall sharply, hammering prices. While trust in Moscow is deeply damaged, economic pragmatism can be a powerful force—especially in energy-hungry, price-sensitive economies.

Europe’s Shift from “Crisis Buyer” to “Phase-Out Mode”

While LNG demand remains high today, Europe has no intention of being this dependent on fossil fuels forever. The EU’s energy transition is accelerating, with massive investments in renewables, energy efficiency, and electrification. This means that by the late 2020s, Europe could be buying far less LNG than it does today—potentially leaving suppliers with a surplus.

A Global Supply Glut Is Coming

Over the next few years, massive new LNG projects in Qatar, the U.S., and Canada will come online, potentially tipping the market into oversupply. If Europe’s demand peaks just as new supply floods the market, LNG prices could nosedive, slashing profits for today’s biggest winners.

Regulatory & Political Risks

Governments are already taxing windfall LNG profits, and new regulations—such as carbon border taxes—could increase costs for high-emission gas producers (like those in the U.S.). Political pressure to accelerate the shift away from fossil fuels could also lead to premature shutdowns of LNG infrastructure, forcing companies to adapt faster than they’d like.

Midstream & Energy Infrastructure: The Unlikely Rock Stars

(Potential Winners: Snam (SRG.MI), Engie (ENGI.PA), Excelerate Energy (EE))

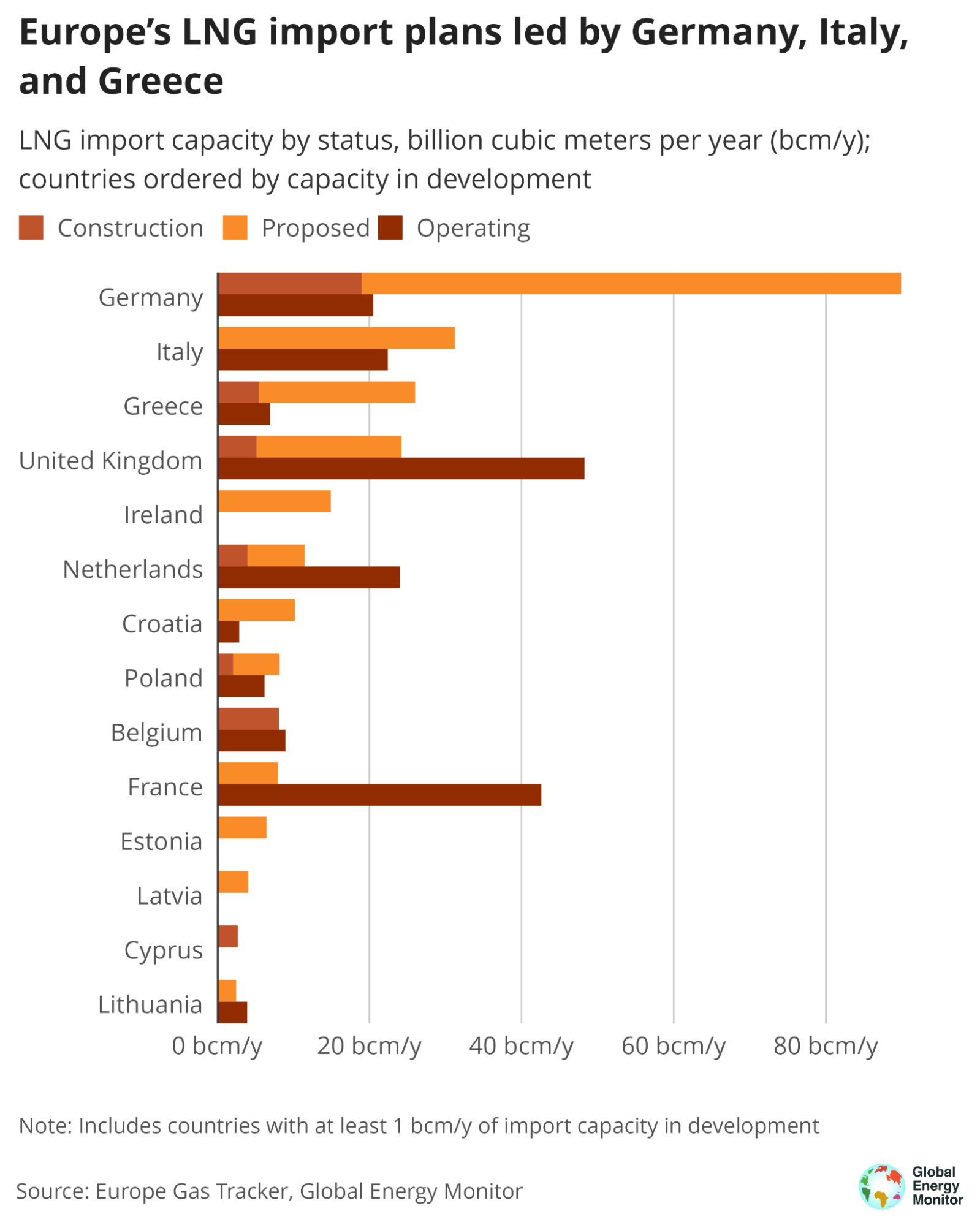

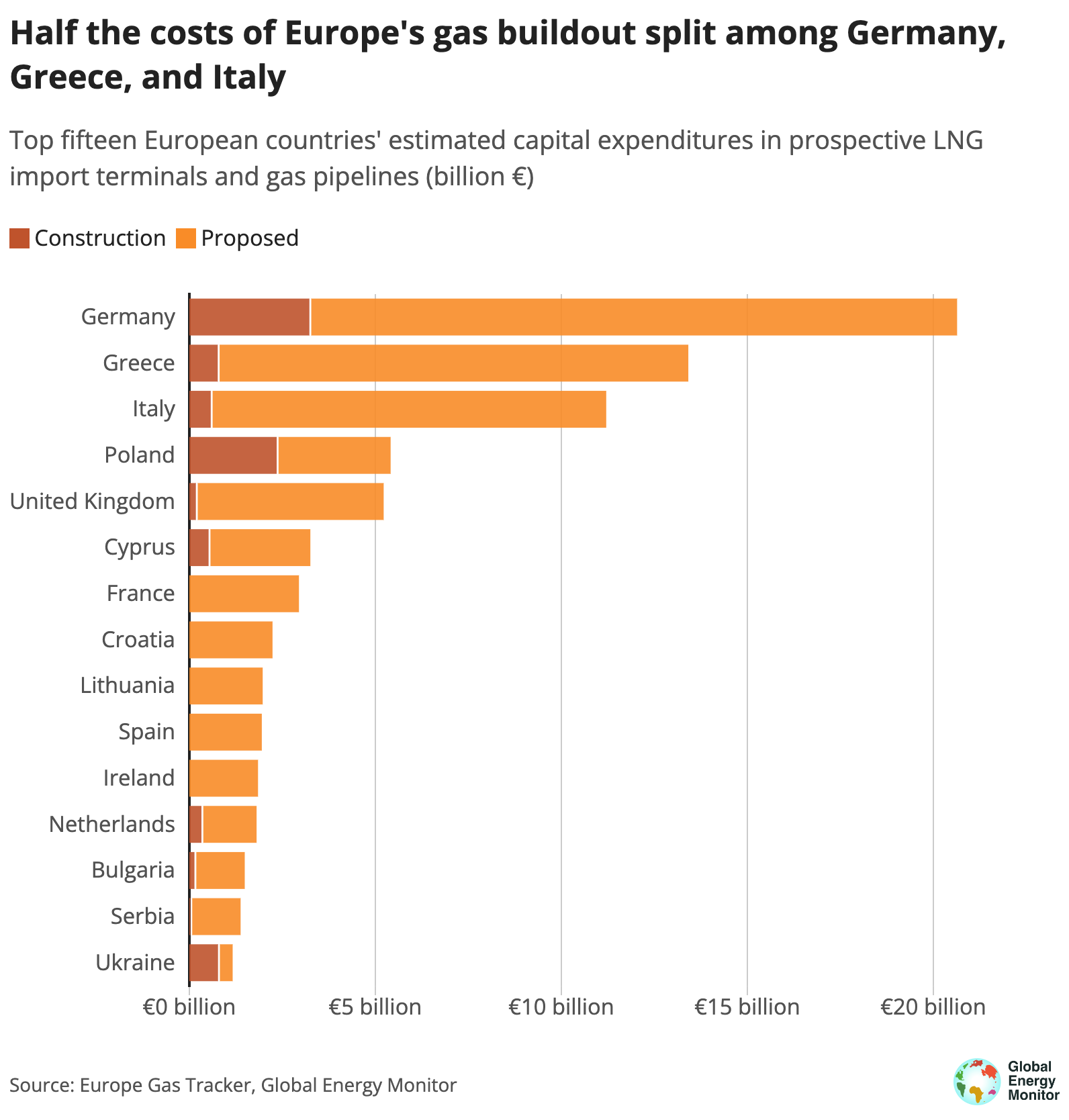

You wouldn’t think pipelines and floating storage units would steal the limelight, but in an era of “sovereignty at any cost,” that’s precisely what’s happening. Italy’s Snam, France’s Engie, and U.S.-based Excelerate (the FSRU specialist) are capitalizing on Europe’s frantic push to plop down new terminals wherever coastline exists.

Why They Benefit:

Europe’s LNG Infrastructure Boom

Europe didn’t just start buying LNG—it built an entire import network from scratch. Governments threw billions at new terminals, storage facilities, and pipelines, ensuring that even if Russian gas returned, they’d never be fully reliant on it again.

Companies like Snam and Engie are now at the center of this transformation, owning and operating critical gas infrastructure across the continent. Excelerate Energy, which specializes in floating storage and regasification units (FSRUs), found itself in high demand as countries rushed to add import capacity overnight.

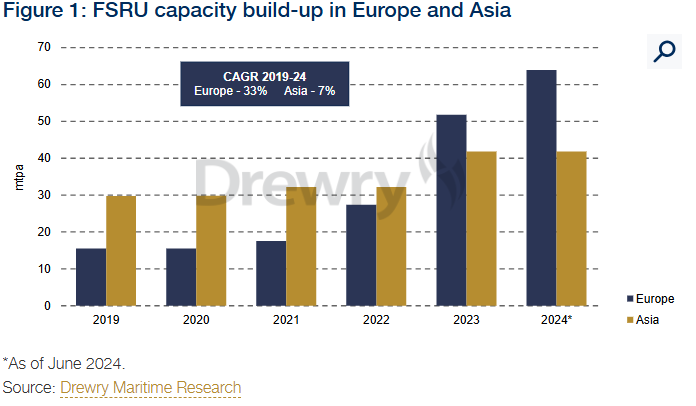

FSRUs: The Ultimate Flexibility Play

FSRUs—essentially floating LNG terminals—became Europe’s quick fix for supply shortages. Germany, Finland, and the Netherlands all rushed to lease them, with Excelerate Energy reaping the rewards.

The beauty of FSRUs? They can be moved. If European demand falls, Excelerate can simply relocate these assets to Asia or South America, ensuring continued utility and profitability.

Market")

Stable, Utility-Like Cash Flows

Many of these infrastructure assets operate under regulated return frameworks or long-term contracts, meaning that even if LNG throughput fluctuates, revenue streams remain stable. For investors seeking low-risk exposure to the energy transition, Snam and Engie offer an attractive, predictable alternative to commodity-price-sensitive producers.

Risks:

Overcapacity and Stranded Assets

Europe may have overbuilt LNG import capacity. If demand falls faster than expected, some of these assets could become underutilized or even obsolete, forcing midstream operators to write down investments.

Demand Destruction from Renewables

As wind and solar scale up, gas-fired power plants will lose market share, reducing pipeline and terminal utilization. Electrification of heating could further erode demand for natural gas infrastructure—a risk that midstream investors must weigh carefully.

Regulatory and Political Uncertainty

European policymakers may decide to cap fees, impose stricter emissions regulations, or even accelerate the decommissioning of fossil gas infrastructure. Midstream companies that fail to adapt (e.g., by integrating hydrogen capabilities) could find themselves at a serious disadvantage.

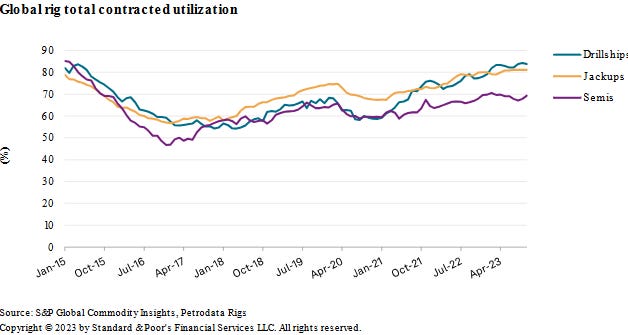

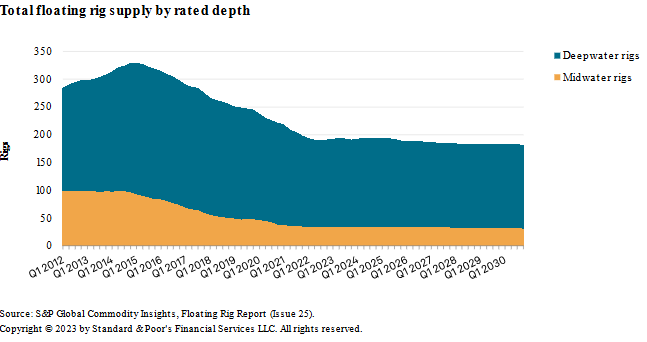

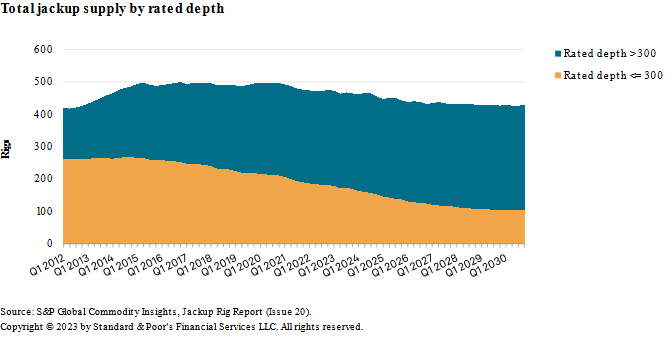

OSV & Offshore Drilling: The Under-the-Radar Upcycle

(Valaris [their warrants are interesting], TDW, SDRL among others) - think this will be one interesting place to allocate for these next 2-3 years

While Brussels preaches “net-zero at any cost,” a quiet offshore revival is charging ahead—driven in part by Europe’s sudden hunger for non-Russian hydrocarbons. Deepwater and North Sea projects are back in the spotlight, ironically powered by the same European majors who pledge green ambitions on Monday and sign new offshore drilling deals on Tuesday. Global rig utilization now hovers near 90%–94%—a stark shift from the 2015–20 glut—while dayrates for top-tier drillships flirt with $450k–$500k/day. Offshore Support Vessel (OSV) operators, which deliver everything from drilling fluids to crew, report 70%+ hikes in charter rates since late 2021. With practically no new rigs or OSVs under construction, supply remains tight and ripe for a multi-year run.

Why They Benefit:

Energy Security Frenzy: Europe’s scramble to replace Russian pipelines has North Sea drilling back on the agenda (climate PR be damned). Meanwhile, European majors like TotalEnergies and Equinor are doubling down on deepwater fields (Brazil, Guyana, West Africa) and need more rigs and OSVs than ever.

Underinvestment Hangover: After years of cold-stacking and scrapping rigs, the fleet is drastically smaller—just as Europe decides it actually needs oil supply. That shortage buoys dayrates for rig owners and keeps vessel utilization tight for OSV firms.

Big Corporate Wallets: Operators flush with 2022–23 oil revenue are greenlighting multi-year drilling campaigns. That locks in rig capacity at dayrates reminiscent of 2014’s heyday, giving OSV providers stable revenue and plenty of headroom to push rates higher.

Risks:

ESG & Cost Inflation: For all Europe’s renewed talk of “energy security,” a quick political U-turn could throttle offshore permits. Meanwhile, reactivating or building rigs is more expensive than ever, so if dayrates don’t track inflation, margins can get crushed.

Oil-Price Wobbles: An abrupt recession or OPEC mischief can sink oil prices. That would freeze final investment decisions (FIDs) on big offshore fields, pulling the rug from under this rig-and-OSV party.

Possible 2027 Oversupply: If rates stay sky-high, eventually someone orders a newbuild flotilla or reactivates cold-stacked units en masse. By 2027, a fresh wave of capacity could dampen the upcycle just when it seems unstoppable.

In the end, Europe’s vow to “move beyond fossil fuels” curiously requires more offshore drilling—particularly if U.S. shale stalls and liquefied gas remains pricey. A well-timed bet on OSVs and rig contractors could pay handsomely if these contradictory policies keep fueling a market starved of modern assets. Welcome to Europe, where a pipeline snipped in the East can catapult dayrates in the West.

The Steel Boom That Just Became a Fizzle

(Potential Names: ArcelorMittal (MT), U.S. Steel (X), Tenaris (TEN.MI)) - 25% blanket U.S. tax might create a great buying opp on EU names…. but keeping in mind demand is weak - no trade here for now

Conventional wisdom said that if Europe was busy building LNG terminals, upgrading defense gear, and resurrecting industrial lines, then steel producers would be popping champagne. Except, in a twist that’s almost too on the nose, the White House slapped a fresh 25% global import tariff on steel and aluminum—just in time to snuff out that optimism.

Why It Still Half-Works:

There is indeed a structural bump in steel demand for defense hardware and energy infrastructure. Companies like Tenaris thrive on pipeline orders, and ArcelorMittal might still see volumes creep up. But coking coal costs could stay lofty if global miners keep underinvesting. While Europe’s steel output might shrink, Asia (especially India) is forging ahead—keeping metallurgical coal markets tight and ironically hiking input costs for EU mills. So, a fleeting uptick in steel volumes could get whacked by expensive raw materials.

Risks:

U.S. tariffs create cross-border friction, hurting mills already burdened by insane Euro power bills. A steel “trade war” could overshadow the underlying demand story, leaving this once-promising tailwind more like a mild breeze. But this might create a great buying opportunity down the line after some pain. I am waiting on this one.

Defense Contractors: Weapons, the New European Language

(Potential Winners: Lockheed Martin (LMT), Raytheon (RTX), Rheinmetall (RHM.DE), BAE Systems (BA.L), Thales (HO.PA), Rolls-Royce (RR.L))

If there’s one bright spot in a region that once bragged about pacifism, it’s arms manufacturing. Germany is plowing a special €100 billion into the Bundeswehr, Poland’s spending spree is off the charts, and even the holdouts are scouring the catalogs for advanced drones or fighter jets.

Why They Benefit:

The rearmament wave is real; Europe’s appetite for American hardware looks insatiable—especially if that’s the only way to dodge tariffs on Porsches and Hermès scarves. Meanwhile, EU-based players like Rheinmetall and BAE soared on tank orders, Thales profits from avionics expansions, and Rolls-Royce supplies the engines that keep fighter jets airborne.

Risks:

A Ukraine peace might reduce urgency, but spooked governments rarely undo defense budgets overnight. So, arms makers might bask in multi-year tailwinds, all while politely ignoring Europe’s prior talk of “peace dividends.”

Bonus round:

Heat Pump Makers: Europe’s Next Holy Grail—or Just Hot Air?

(Potential Winners: NIBE Industrier (NIBE-B.ST), Daikin (6367.T), Carrier Global (CARR) - Carrier is best positioned here and benefited from a Trump Election pullback for entry-demand is not going anywhere for now though. The first two are higher risk recovery plays.

You’d think Europe’s big dream—kicking natural gas out of every house in favor of sleek heat pumps—would be the triumphant badge of “energy sovereignty.” Naturally, that’s turned into a messy scramble of subsidies, new regulations, and a frantic wave of consumer confusion: “Wait, I have to replace my boiler with a what?” Enter the heat pump makers, who stand poised to convert Europe’s fear of gas bills into scorching sales. But dig deeper, and you’ll find some drafts of reality wafting through the hype.

Why They Benefit

Europe’s “No More Gas, Ever” Obsession

Brussels and countless national governments have unleashed a flurry of pledges and deadlines to ban new gas boilers by 2025, 2027, 2035—pick a year, any year. Even if half these mandates slip, that’s still a colossal market for heat pumps. Every homeowner who used to sign up for a shiny new gas boiler might be forced into a heat pump unit. Manufacturers like NIBE and Daikin are practically licking their chops at the legislated demand.Subsidy Candy

From Germany to France, subsidies for installing heat pumps can reach thousands of euros, turning home retrofits into a discount bonanza. Governments want to brag about “decarbonizing home heating,” so they’ll shovel money at anything that hums on electricity instead of gas. Providers who can jump through the bureaucracy hoops get to charge top dollar—sorry, top euro—on systems suddenly made affordable by taxpayer generosity.Rising Electricity Reliance

The old fear was that electricity prices might cripple heat pumps’ advantage. But with pipeline gas no longer cheap (thanks, Russia!) and Europe frantically building out more renewable capacity, policymakers are banking on stable-to-lower electricity costs. If that bet holds true, it cements the operating-cost argument for heat pumps. Manufacturing margins improve as volumes scale, creating a tidy virtuous cycle—for the pump producers, at least.Eco Image + ESG Capital

Heat pumps are the new ESG darling. Even if they’re powered partly by coal-tinged grids (who’s checking?), they’re still sold as planet-saving upgrades. As a result, big institutional investors with net-zero pledges like plowing money into “clean tech” stories. Heat pump makers can ride a wave of cheap capital to expand capacity—even if the actual carbon math is a bit fuzzy.

Risks to Keep in Mind

Grid Strain & “Oops, The Power Went Out”

Replacing millions of gas boilers with electric devices is sort of like hooking a thousand new Tesla Superchargers into local distribution grids. Are those wires up to snuff? Maybe not. If winter demand spikes and local grids can’t cope, expect frantic political finger-pointing—and potential slowdowns or halts in new heat pump mandates. Nothing kills a policy craze faster than rolling blackouts.Pricey Installations & Sticker Shock

Sure, subsidies help, but heat pump installations can run double or triple the cost of a boiler, especially in older homes requiring major insulation. People might balk—even with rebates. There’s a real risk that once the first wave of “eco-passionate” homeowners is done, mass adoption stalls unless governments keep sweetening the pot. And if budgets tighten? Goodbye lavish subsidies, hello resurgent gas boilers.Raw Material & Supply Chain Hiccups

Heat pumps need compressors, refrigerants, specialized electronics—and a ton of copper piping to move heat around. If supply chain drama rears its head (again), or if raw material prices surge, these units get costlier to produce. The industry can pass on higher costs only so far before politicians cry foul or consumers run for the cheapest alternative. Meanwhile, new environmental regulations on refrigerants could force pricey design changes, hammering margins.Possible Tech Shifts & the Hydrogen Wildcard

A few years ago, hydrogen boilers were the Next Big Thing—some governments still flirt with that idea. If hydrogen or another magical technology emerges (or if Europe invests heavily in hybrid solutions that keep partial gas usage), the heat pump mania could deflate. Companies that bet everything on heat pumps might be stuck with warehouses of specialized parts no one wants if policymakers pivot again.

Cheers!

Drop a <3 if you found this interesting!