The great growth scare of 2024 that lasted a long week has been averted thanks to 7000 brave souls who are enjoying a life with solar panels, a Tesla, the latest AI-powered iPhone, and rock an H100 GPU for their casual gaming with no need to file an initial jobless claim. We are truly seeing the miracle of sustained growth and prosperity for all unfolding before our eyes!

But anyway, the silliness of the markets aside… let’s look at what is actually going on with economic growth and chart a path forward with the hopes of generating some risk-adjusted gainzzzz.

The Fed has generally maintained, before the Covid-stimulus an implied lower bound of 100bps of Fed Funds over CPI. This target should be expected to be a point of convergence maintained inflation continues to show signs of abating as long as economic growth remains positive. Real rates currently sit at a 2+% level which indicates the quantity of rate cuts that we can expect within this cycle. If the economy starts a contraction, the Fed would have a reason to reduce that implied target spread but we are not there yet. It is important to appreciate the reaction function of the Fed toward setting the policy rate relative to inflation and growth. Given a growth rate, the policy rate will parallel shift along with inflation. Given fixed inflation, a reducing growth rate reduces the spread between the policy rate and inflation, this second relationship is harder to quantify (it is policy and not math after all) but remains directionally correct. It is this tension between growth and inflation that the market is implicitly extrapolating. In this primer, we will set the foundations of understanding the direction of growth and inflation starting with balance sheet-driven monetary policy and consumer health.

So… what are the components of economic growth indicating and what is the dispersion in signal between these indicators? Over the last few months, there has been a sprinkling of negative economic data which increases the number of paths to reach a recessionary environment. Quantifying or at least qualifying the probability that these paths come to fruition will be the exercise we need to perform independent of market reactions to position our portfolios over this cycle and tactically benefit from mispricing such as that of the great yen-carry-trade-unwind-Monday (mispricing is not quite the right word but will make a primer on carry trades and how clearing houses exacerbate their unwind later).

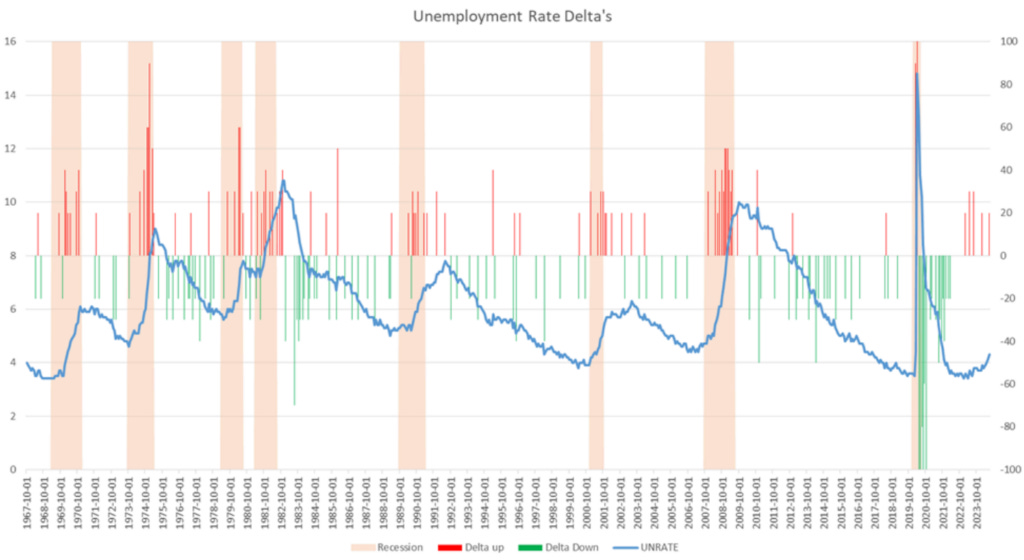

One question we will need to keep an eye on is how persistent will unemployment be. We have seen in history several 20bps+ print increases from the prior month which have not led to recessions, since 1967, 45% of such prints have not been in periods of recessions; a good chunk of those are in periods of broadly stable or decreasing unemployment. Now… not a very useful statistic to gamble our money on but gives us time to think about the components of growth and GDP.

And yes, I have known about Sahm’s rule since last week when it became relevant but I like to KISS (Keep It Simple Stupid) and stick to first principles.

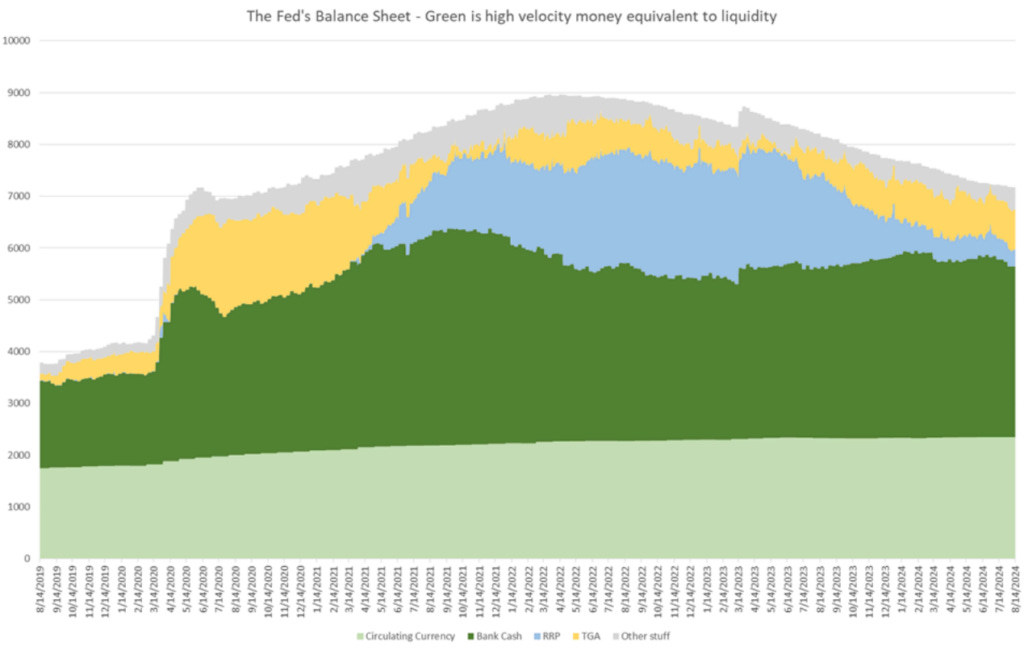

The monetary easing cycle has already started about a year ago with the Fed discreetly waving its balance sheet arm under our noses and providing a supportive environment to risk assets. This may seem somewhat counterintuitive given the Headline QT to combat inflation the Fed has been implementing to which continues albeit at a slower pace since June ($95bn to $60bn per month). The topline number for the Fed’s balance sheet is contracting peaking at $9tr in Aug 22 and now at $7.2tr, however the make of the Fed’s accounts has resulted in a net easing of financial conditions.

Let’s go through liquidity mechanics to appreciate the monetary easing taking place given the data today.

The monetary base is composed of money held by the public and commercial banks while the treasury general account (TGA) and Reverse Repo Facility (RRP) reflect money held by the Fed. The monetary base provides a better picture of liquidity in the system as it is effectively high-velocity capital that is ready to be deployed for economic activity and investments. The dollars held at the Fed are removed from the financial system and do not provide liquidity to banks and by extension, are not in circulation and being used for economic activity.

The amount of liquidity in the real economy or high-velocity money is principally affected by the interactions between QE/QT and the treasury’s debt issuance via the TGA. Headline QT is the process of letting UST's expire on the FED’s balance sheet and the proceeds not being reinvested. Here the treasury is paying the central bank from its TGA account which is held at the Fed and with sufficient outflows from the TGA, the treasury will be forced to issue more debt removing liquidity from public markets, hence tighter financial conditions. When the treasury issues debt funded onto its TGA account, that debt issuance can either be absorbed by the FED such as during the Covid stimulus which then circulated into the economy and adds liquidity by moving dollars into the monetary base/into the hands of the public, corporations and banks as the federal government spends this money raised by the FED or it can be absorbed by the public market reducing liquidity in financial markets, raising bond yields and gradually easing as the government deploys spending. QT on the UST’s can be visualized as a leak from the TGA onto the FED’s black hole which then needs to be filled with additional debt, this additional debt is money from the public which moves onto the FED’s low-velocity money balance sheet. The same process can be done with MBS directly targeting homeowners and therefore reducing cash on hand at commercial banks.

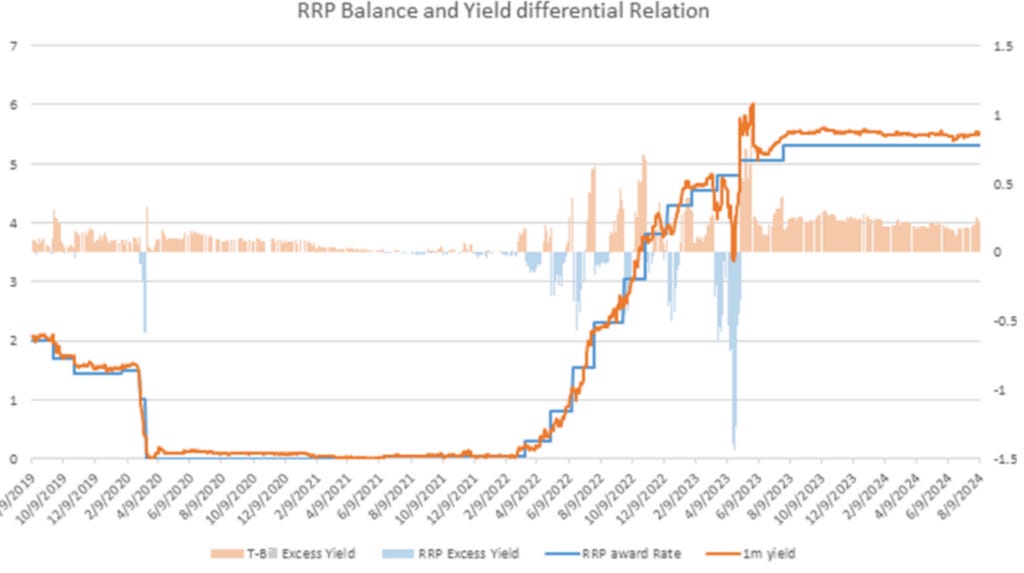

The issue with QT and QE is that the magnitude of the impact on the economy is unknown especially since its impact can be altered by fiscal policy. With QE for example, there is a point where so much cash has been added to the system that rates on the short end go to zero and eventually flip negative. To solve the magnitude problem organically, the overnight reverse repo facility allows market participants to give money back to the Fed at a set award rate (since June 2021 moves in lockstep with rate hikes/cuts and was 0% prior) instead of absorbing lower yields. The RRP behaves like a sponge for excess liquidity and effectively reduces the quantity of dollars that would otherwise be circulating in the monetary base putting a floor on yields. By definition; the RRP has no credit risk and no duration risk; which implicitly targets money market funds that have a goal of being completely risk-free across duration and credit and redeemable at par. The RRP is by construction the best investment for MMF’s above Treasuries given an equal yield.

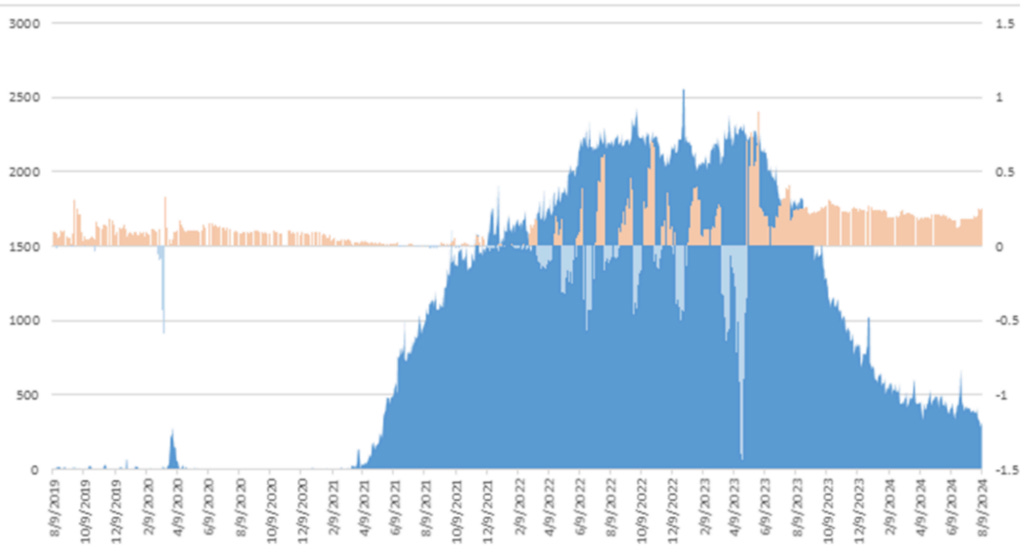

During the easing cycle post covid, the RRP balance grew from 0 to $2.5tr from early 2021 to early 2023 and represented about 30% of the Fed’s balance sheet. This effectively absorbed the stimulus from QE during that period. On June 1’st 2023, through congressional wrangling, the debt ceiling was lifted (surprise surprise) to avoid a technical default and allowed the treasury to issue T-bills (short-term debt) and fill the gap left by COVID-19 stimulus in the TGA. Part of the reason for issuing T-bills in particular is to avoid locking in higher rates with longer duration given the anticipated rate cuts and maintaining stable long-duration yields. The constant supply of T-bills into the market caused yields on the short end to rise above the policy rate for the market to absorb the increased issuance. Due to the excess supply, the bond yield has stayed above the RRP award rate which created a draw away from the RRP by MMF’s adding to the volume of high-velocity money in the economy and raising liquidity in the system offsetting the tightening caused by QT and Treasury bond issuances to the public markets.

The RRP now sits at a measly $400bn of balance. This mechanism of the RRP and its interaction with the TGA has effectively been supplying the market with a constant bid on T-bills away from the RRP, offsetting the liquidity drain from new treasury issuance in addition to QT. At the current rate of $60bn in tightening, the RRP has enough capital to keep the total Fed balance sheet constant and offset/funds QT for another 8 to 10 months. The RRP will only function as long as it is funded; as we approach it being emptied, the FED will be forced to reduce the speed of QT further or simply stop it to avoid subsequently reducing bank reserves. I expect this to be announced in tandem with the first anticipated rate cut in September.

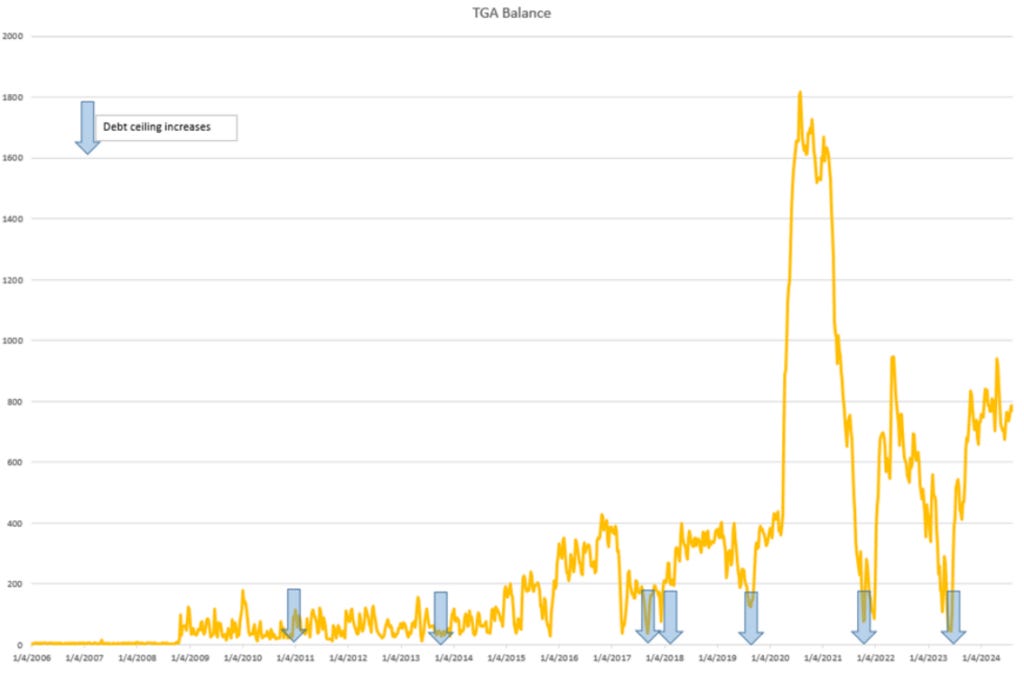

Another source of balance sheet easing we can expect to kick off in 2025 comes from the potential shrinking of the TGA balance which incidentally is also inflationary, hence the importance of having hedges across the various paths the economy can take. Taking the TGA balance out of the first plot in this section helps us appreciate the mechanics we can expect given the natural behavior for the TGA and what can be anticipated from the coming election results.

Currently, there is no debt ceiling on the national credit card until the start of next year, however, Supreme Leader Yellen dictated that she will maintain the same balance through this period. When the unlimited credit card runs out, the treasury will be obliged to eat into its cash reserves reducing the TGA and directly injecting liquidity into the real economy (and indirectly into the pockets of the elite with rising asset valuations). Neither Trump nor Kamala are keen on reducing spending, hence this process should be fairly speedy and supportive to asset prices in the first half of 2025. We can moreover predict the next haggling over the debt ceiling to happen in Q2 of 2025; should be fun TV! In the meantime Yellen will do her part to prop up the US economy by stimulating consumer spending, she probably singlehandedly helped raise retail sales by 1% above all estimates this glorious Aug 15th.

Furthermore, the regional bank crisis forced a rapid liquidity spurt into the banks through the term funding program, increasing cash assets and reducing leverage. This ameliorated the health of the banking sector stimulating the origination of credit at some ~2% annualized despite higher rates. This has been another source of effective easing in the economy.

These effects have been broadly supportive of liquidity in the economy, the creation of credit, and by extension supportive of the cyclical valuation risk assets which are set to continue.

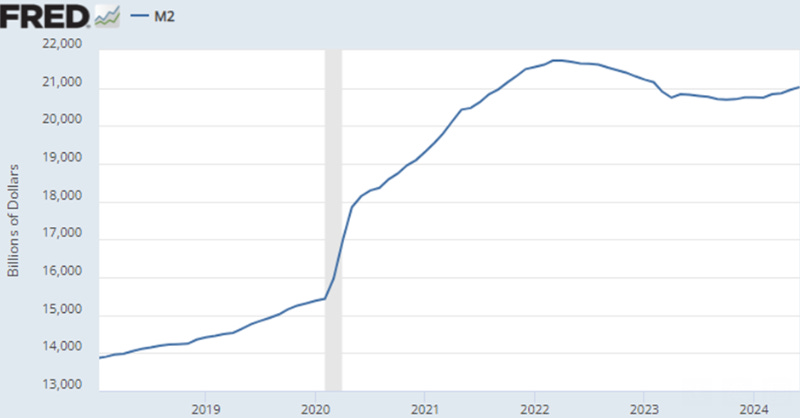

What is the net effect of all these shenanigans on the monetary base (M2)? We see through 2024, the circulating amount of money steadily increasing which reflects the net easing the economy has experienced during this period of monetary tightening.

Simultaneously we have also seen an acceleration of corporate credit originations and equity raises, a consequence of easier money circulating the economy.

Next post for part numero dos on the consumer

Cheers!