What is the likely path for growth now? – What is my credit card limit?

How has Yellen’s shopping been doing?

We have covered some monetary theory in the prior post to understand the net easing the economy has effectively seen in a period of relatively tight monetary policy.

What is the underlying growth story?

One of the issues with how economic data is presented comes with the one-dimensional semi-binary view taken at each print within the good news or bad news is bad news or good news or vice versa or contrapositive or something to the point where a 7000-person difference between realized and expectations in unemployment claims numbers ushered in the end of the great growth scare of 2024 which lasted 5 days on the back of a 20bps worse unemployment number than expected a week prior which was still well within the margin of error for the estimate. Taking a more complete view of the economy and its drivers should help position trades and investments to generate excess risk-adjusted returns over this cycle and understand what proportion of the portfolio should be allocated to adverse scenarios caused by a pickup of inflation, deflation, growth slow and maybe recession while knowing the answer won’t be buying puts on NQ during a selloff.

I’ll focus this first primer on the consumer broadly as he is a core component of the economy (which is made of people in addition to GPUs). A 70% of economic activity in the U.S. is driven by consumer behavior. Later primers will provide a framework to relate consumer trends to growth and we will dive into the various industries that make the economic landscape.

The Consumer

To understand the current state of the economy and estimate which sectors are set to outperform this cycle, we need to take a look at where everything starts… the American consumer. After all, what’s the point of credit card debt if not to buy H100 pro max’s?

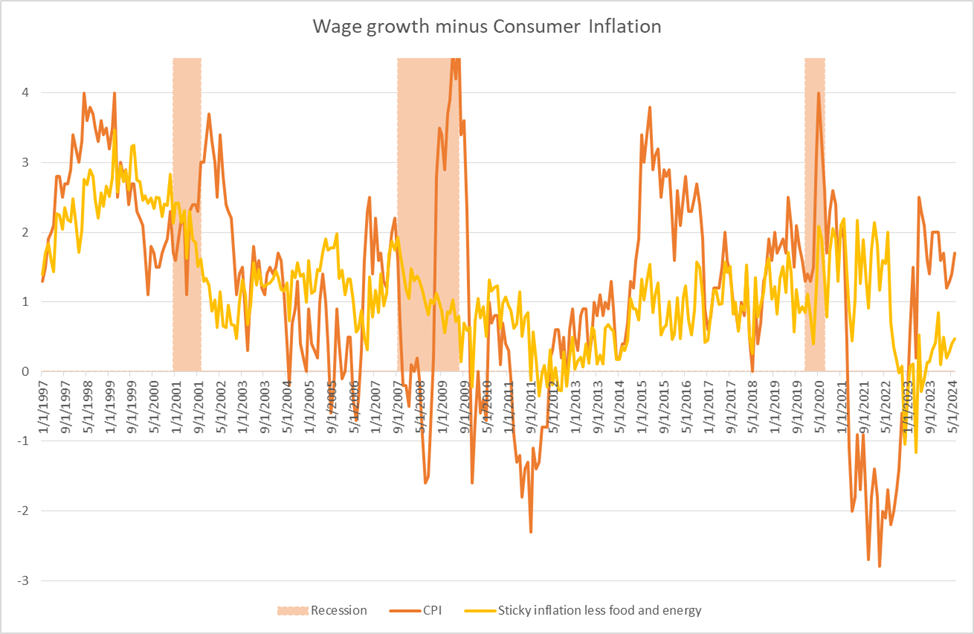

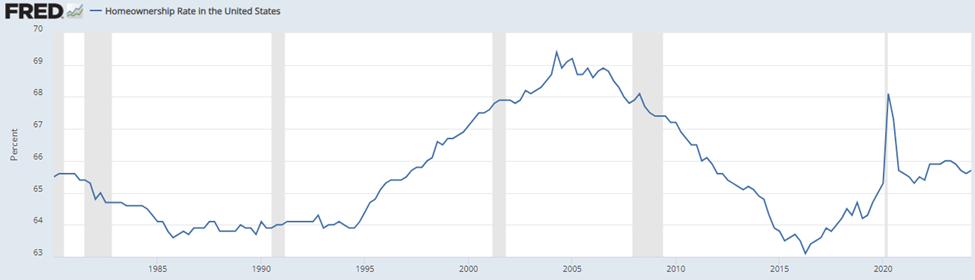

Before looking at debt, it would be useful to know if the American spender has the ability to spend. Wage growth is one of the key metrics to appreciating the health of the consumer relative to inflation. If costs of goods outpace the ability of earners to increase their wages, we can expect to see a longer-term contraction of spending and investments in durable goods. Currently, we are observing a continued recovery of real wage growth from peak inflation in mid-2023 indicating a capacity to support spending or accrue wealth. This should be supportive to also see an increase in the percentage of homeowners in the US which has flat-lined since covid as mortgage rates come down; we are already seeing refi’s more than double on the pricing in of rate cuts.

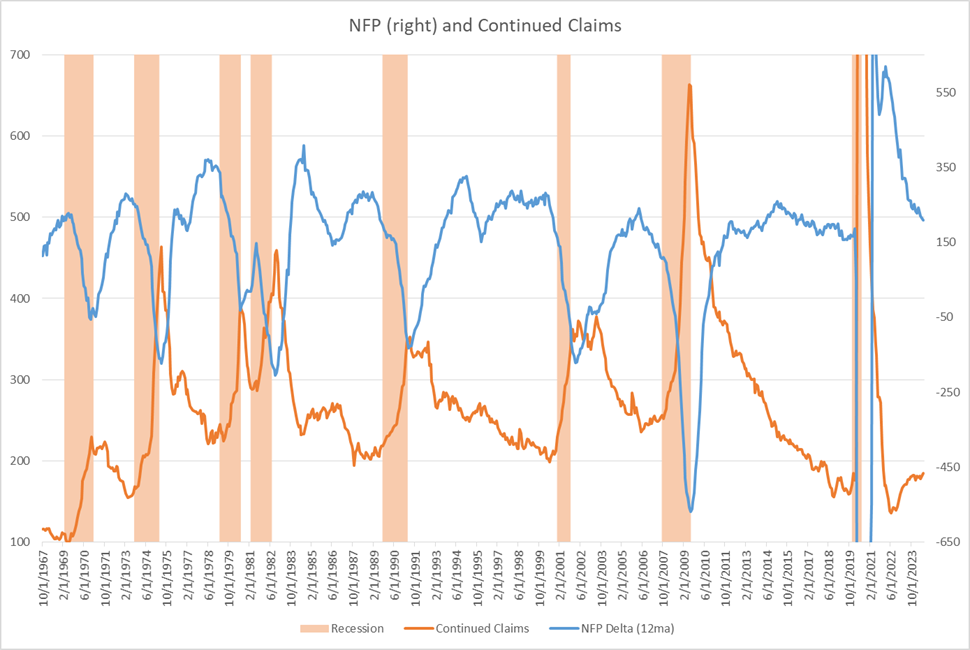

We also should get a handle on the job market and try to extrapolate if the current disinflationary impulses should lead to sustained decreases in job creation and potentially job losses while also getting a sense of job quality.

U-5 is the official rate plus discouraged workers

U-6 is basically U5 plus part-time workers for economic reasons, I think there is value in looking at the three together as part-time workers who would otherwise prefer to have a full-time job also are an indicator of weakness in the economy. We see however that the delta between U6 and the other two measures remains relatively constant at the level before covid and through the health crisis, so we can focus on the changes in the official measure.

Now despite unemployment ticking up, jobs are still being added to the economy but at a decreasing rate which we see with the Non-Farm Payroll numbers which is indeed what we expect to see during recessions. The caveat here is that the starting point for the NFP numbers is artificially high due to the post-COVID surge and is currently well within the expected NFP adds we see during periods of growth. For now, we should expect NFP’s to move towards pre-covid levels (150+ from the current 170) without necessarily implying the beginnings of a recession but rather the expected slowing of growth from fighting inflation using monetary policy. A similar story from continued claims that are creeping up back towards the pre-covid levels which should be expected from the normalization of the economy that we are seeing. Now this does not preclude that the economy overshoots towards deflation.

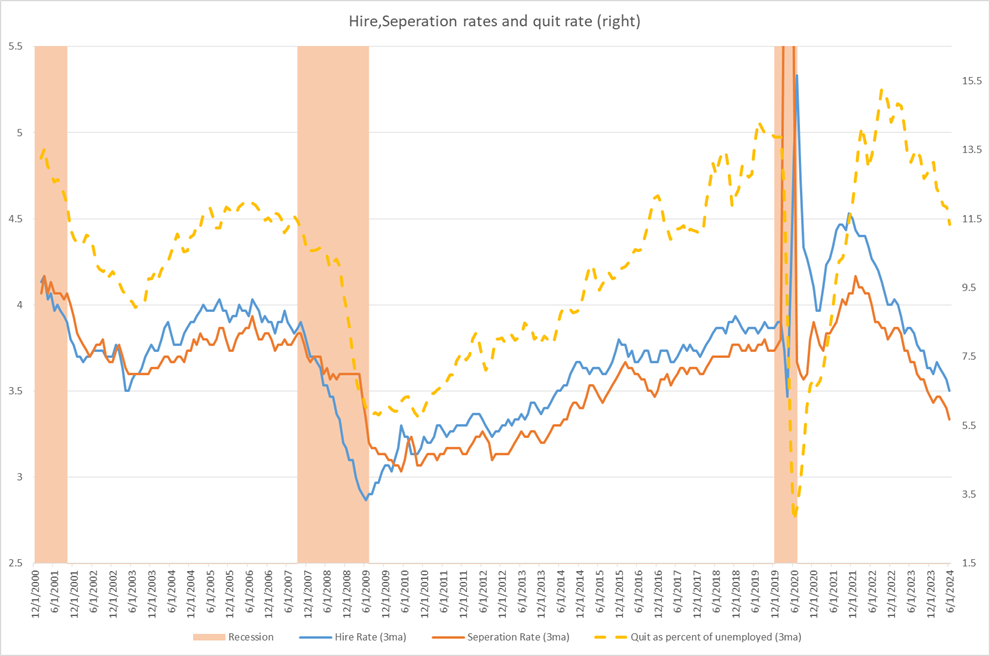

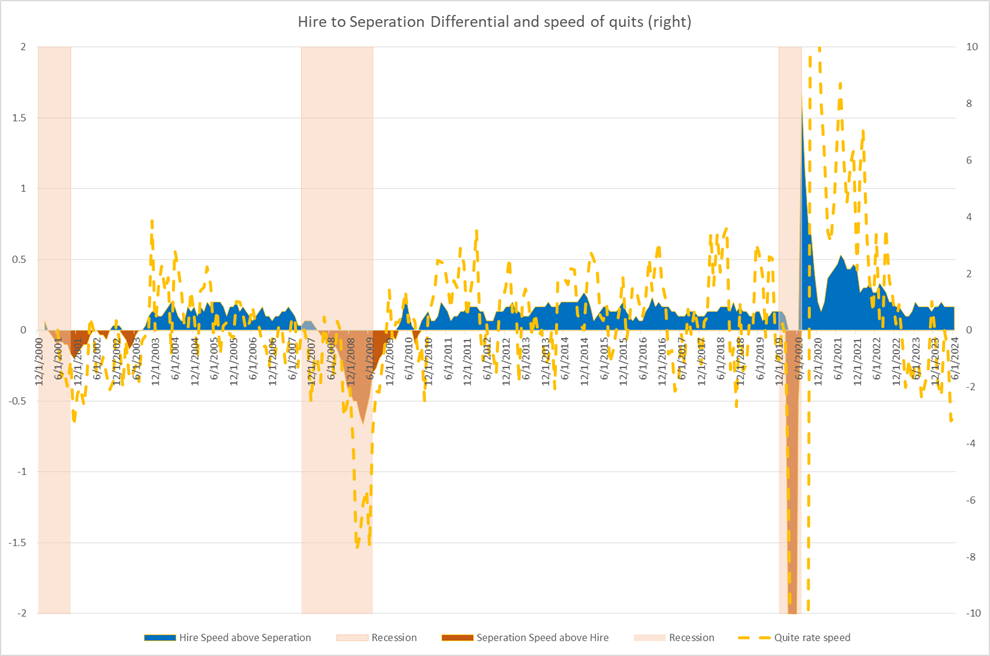

Another view on the rate of employment which provides a notion of the speed of job creation and employment in the economy comes from the hire rate, separation rate, and the voluntary quit rate as a percent of the unemployed population. The Hire and separation rate is calculated with the employed population as the denominator where separations reflect voluntary and involuntary.

First, we note the employment and separation rates are at the levels seen during the 08 financial crisis.

Ok, time to stop writing this and blindly press the big red sell button…

But wait we are currently in a situation near maximum employment so the denominator being looked at is substantially different. Moreover, during the GFC, the separation rate exceeded the hire rate, which we are not currently seeing. So what is this parallel decline in both ratios telling us? Well not quite sure without looking at a third metric, the voluntary separations as a ratio of the unemployed population which is in decline but now at levels before the health crisis.

As a general rule, if jobs offering better opportunities are harder to come by then we should expect the rate of people resigning from their jobs voluntarily (excludes sickness and retirement but does not exclude extended holidays to write this primer on the banks of a Vietnamese river) to be declining. This is reflecting a weakening of the job market where opportunities are harder to come by, however, within the context of almost full employment, an economy with positive but slowing growth should be expected. One thing to look for will be then the hire and separation rates flip with an acceleration and persistence in the decline of the quit rate. One caveat for using this indicator is it’s backward-looking nature, rather when it flips your hedges should already be in the money.

How has Yellen’s shopping been doing?

By today’s account, more than well! She probably went out on an H100 shopping spree! However looking historically, we notice that the month-on-month retail spending number is highly oscillatory and not quite the indicator of good and bad times for the economy. The year-on-year number is much more interesting and shows easier-to-distinguish trends for us making gambling decisions by eyeballing charts using the fundamental and self-evident natural laws of technical analysis. We observe that on a year-on-year basis, the US consumer is consuming incrementally less but is still putting to good use the real wage growth we have observed previously. It will be important to monitor all the prior metrics in conjunction with this one to evaluate the health of the US consumer bearing in mind much of these indicators would be fundamentally backward-looking, so also understanding the interactions between these elements and extrapolating their likely path forward is key.

We are currently in a cycle of decreasing growth, positive real wage gains but at a decreasing pace, jobs being added to the economy but the quality of the jobs diminishing, and with spending keeping up but slowly relative to what is desired by our technocrats… Maybe a chance for the consumer to become a saver, but who am I kidding? Look at the next chart…

The American consumer has been building up a bad habit of saving less and less of their disposable income, now at a measly 3.4% creating less resilience in the long term to economic weakening. So my story above is not all daisies and roses and implies that the gamma on economic health is quite accentuated (if I may permit myself to make derivatives references and pretend to sound smart) and skewed to the downside. Now I can’t blindly blame the consumer for their saving habits, rising costs play a large role in the ability of individuals to save.

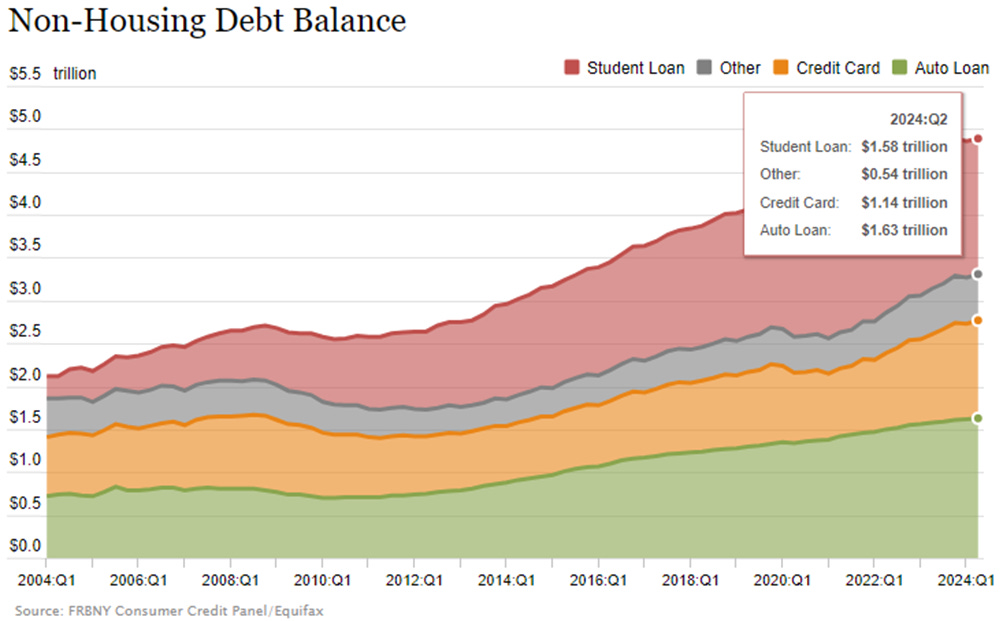

Now, what is the consumer without all his debt?

Before anything, it will be good to contextualize the composition of debt within a household. I’ll let the graphs speak for themselves.

First looking at the quarterly debt service payment on disposable income, we see a very optimistic trend here. Despite higher rates, the share of disposable income eaten up by debt is at historical lows outside of the covid helicopter money period.

This implies that the effective debt burden of the American consumer is manageable historically speaking sitting at 7.8% of disposable income. Note that the numerator here includes scheduled interest and principal payments. Looking through to mortgage and consumer debt service individually we note that mortgage payments have a substantially smaller burden on the average consumer while consumer debt burden is substantial and represents 60% of the total burden. In a subsequent deeper dive into the consumer, we will break down the split between “social class” and the individual debt burden and look to understand the shape of this distribution between mortgage and consumer debt burden by economic status. What I expect to see is that consumer debt is skewed towards those in more difficult economic situations while mortgage debt is skewed towards those who are better off while reminding ourselves that mortgages allow for the creation of wealth while consumer debt does not have such a clear path towards creating equity. If that hypothesis is confirmed that poses a serious question as to the resiliency of the US economy. The overall picture however remains supportive of growth and wealth accretion broadly.

This picture of the debt service also helps explain delinquency trends diverging between mortgages and consumers. The divergence should be further explained by the hypothesis on economic status and the make of debt.

We currently observe that mortgage delinquencies are stable at the 2.5% level which is a historic lower bound on the metric.

On the other hand consumer debt delinquencies have been on the rise, with the curious observation that credit card delinquencies are highly concentrated in small banks. This data point will come to be useful when we construct a long/short good and bad banks framework at a later stage.

I would not posit that rising consumer delinquencies are excessively worrying at this point as we will need to study its distribution across different segments of the population but are certainly a sore thumb in the overall narrative and demonstrate a weakness in the overall economic picture.

The overall picture of the consumer landscape does not immediately point towards a recession and when we broach more explicitly its relation to growth, should see that growth scares are currently excellent opportunities to tactically enter equities at improved valuations within the sustained path upwards which I expect through the end of the year and potentially into next year barring any events carrying substantial entropy.

In the next section, we will discuss growth specifically and inflation trends, and one key downside scenario to the economy, unless I change my mind and feel it timelier to write about something else.

Cheers!