The Roundtable Hold of EU Trades - Peace in Ukraine

Browsing the trade opportunities offered by a continent that focused on the side quest

So there we sit, mon ami, with our espressos going cold, watching a spectacle not a single European leader—nor poor President Zelenskiy—saw coming: President Trump 2.0’s entourage kicking back with Sergei Lavrov in Riyadh, politely drafting a plan to end the war in Ukraine. Yes, Ukraine, whose president wasn’t even invited—perhaps a clerical oversight, but one that spurred Zelenskiy to cancel his own Saudi trip in protest. The bigger irony is that the occupant of the White House seems convinced he can wrap up a war unilaterally, as if the side that started it can sign off without the side still fighting it. Yet from the markets’ vantage point, even a hint of a ceasefire—real, half-real, or purely rhetorical—can’t be ignored. Any sign of calm can jolt everything from airline plays and Eastern European banks to chemical giants thirsting for stable gas supplies.

In a bid not to look thoroughly irrelevant, Emmanuel Macron rushed to convene an “emergency summit,” which, if we’re honest, resembled more of a book club lamenting how the main event was happening halfway across the globe without them. Meanwhile, Secretary of State Marco Rubio, National Security Advisor Mike Waltz, and envoy Steve Witkoff flashed smiles in front of cameras, tossing around phrases like “lifting sanctions,” “ending conflict,” and “future cooperation.” One wonders if the occupant of the White House is aiming for a foreign-policy victory lap before Macron can even say “sacrebleu.” But if calm does emerge—sending markets sprinting into “peace-trade” mode—it’s worth owning a bit of tactical risk on our books. After all, illusions of sovereignty aside, Europe’s crises are a fertile ground for trading opportunities.

Mean Reverting War Premium

Ever since Russia ramped up its offensive in 2022, the consensus was that sky-high energy costs and a booming defense sector were here to stay. But if the occupant of the White House manages to cut a deal that actually stops the shooting, all those assumptions might get tossed in a hurry. A credible ceasefire could entice investors back into Eastern European and German markets—long hammered by conflict jitters (and energy policy regrets)—especially given Europe’s comparatively modest valuations (around 15× earnings in the Euro Stoxx 50 versus almost 27× for the S&P 500). Of course, defense names and utilities enjoying windfall margins might take a hit if rearmament mania wanes, and none of this is guaranteed to last if Zelenskiy refuses to sign off on a pact that overlooks Ukraine’s core interests — let’s not forget Ukraine gave away it’s nukes for security guarantees.

Still, even the hint of peace can reshuffle capital flows in a hurry, and easing tensions might soften Europe’s elevated energy premiums—though it won’t magically piece together its energy puzzle. (For a deeper dive into these entrenched energy issues, see my prior article, “The Roundtable Hold of EU Trades – Greens With a Side of Thermal” where I dissect Europe’s reliance on imported fossil fuels and the region’s patchwork approach to renewables.

Meanwhile, should the occupant of the White House succeed in trimming the U.S. trade deficit or gently weakening the dollar, a shift of investors toward cheaper non-U.S. equities could help narrow the stubborn valuation gap. That might sound like a green light for broad ETFs such as VGK or FEZ, but splashing money across Europe may leave you overexposed to sectors that thrived purely on wartime realities. A more targeted approach—picking companies set to benefit from resumed trade routes, cheaper gas, and recovered consumer demand—might serve you better.

More arguments for the convergence of valuation multiples between U.S. equities to Non-U.S. equities can be found here:

For note, any idea expressed below I am setting up with 6 month to 1 year options and depend highly on an agreement in Ukraine being hammered out. The total premium across all ideas maxes out at 2.5% of NAV and I intend to not let the size grow above 3% after which I take profits (or let it whittle away into nothingness).

European Industrials: Flirting with Cheap Gas

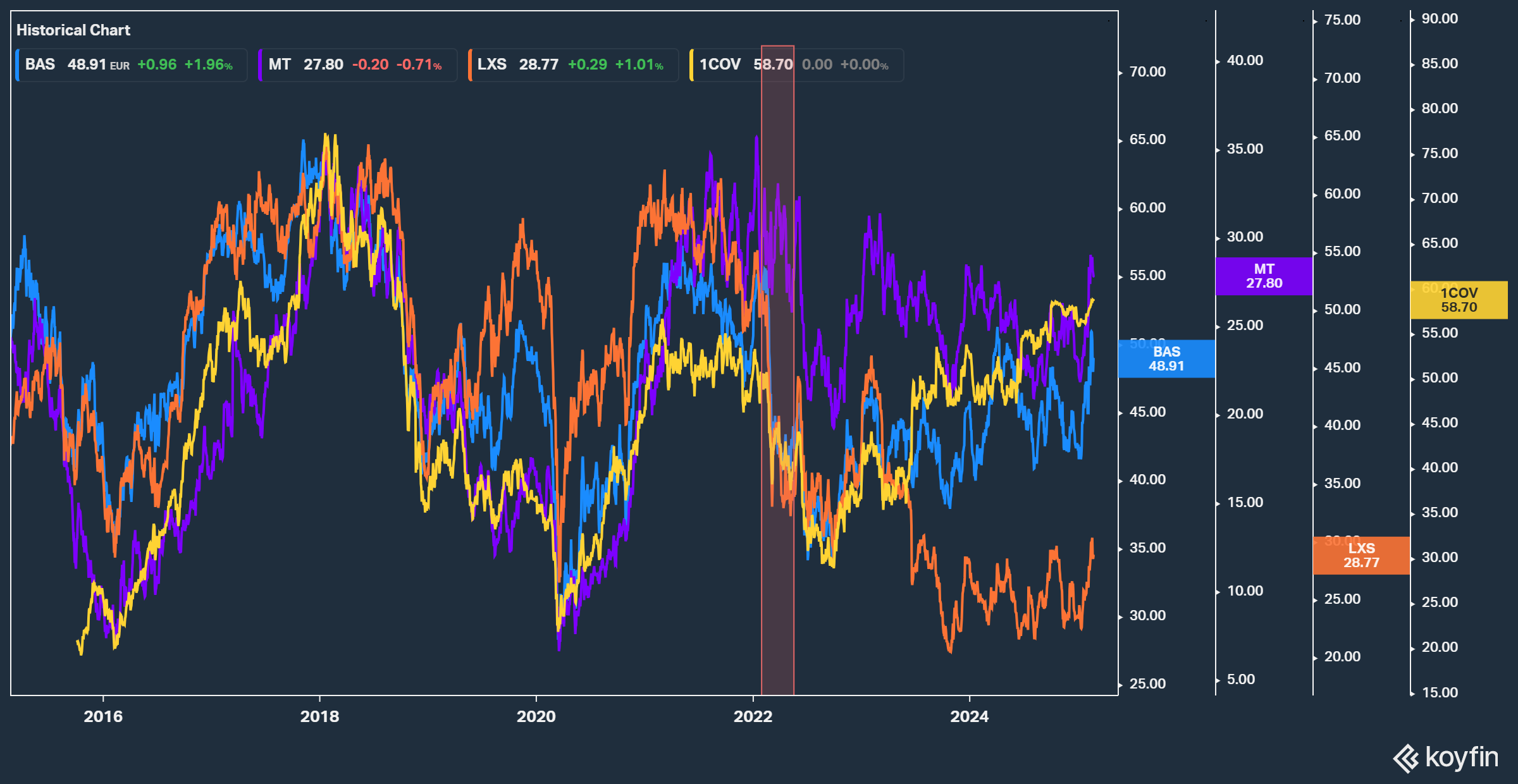

We’re rummaging through the numbers, tracing how Europe’s 2022 energy crisis hammered core industrial output and prompted unprecedented cost surges across steel, chemicals, fertilizers, and building materials. Even as we enter 2025, the aftershocks remain visible in financial statements. By Q3 2023, many energy-intensive sectors still showed pronounced revenue declines versus the early-2022 highs—Lanxess’s 2023 sales sank 17% to €6.71 billion, Covestro’s top line fell ~20% to €14.38 billion, and BASF’s revenue slid 21% to €68.9 billion, well below its €87.3 billion peak. Profits likewise remain subdued. Covestro’s EBITDA for 2023 slipped to about €1.08 billion, further pressured by a second consecutive net loss in its European operations, and ArcelorMittal’s EBITDA halved in 2023–24 from the $14 billion range. Some companies, like Lanxess, managed to boost free cash flow by slashing expensive inventories built up when gas prices soared, yet many continue to see net income near breakeven or below historical averages. Although 2024 brought partial relief, with European gas costs easing from their 2022 extremes, the damage to margins and capacity lingered. EU industrial gas usage in Q3 2022 was down ~25% year-on-year, leading to a roughly 8% output dip in fertilizers, steel, and base metals that carried through 2023. Europe even became a net importer of chemicals for the first time on record. Surveys show 25% of German chemical companies and 16% of automakers cut production in 2023, with some only slowly restoring volumes through 2024. Meanwhile, smaller operators—in aluminum smelting, zinc refining, or glass—either closed permanently or operated at half-capacity just to avoid repeating the meltdown that hammered them two years prior.

On the “unhedged” or heavily exposed side, ArcelorMittal (AMS:MT), Covestro (ETR:1COV), Lanxess (ETR:LXS), BASF (ETR:BAS), and Heidelberg Materials (ETR:HEI) continue to show muted results, with recurring references to how 2023–24 sales and earnings remain 10–20% below pre-crisis levels. Covestro reported a near-20% top-line decline in 2023 and posted another net loss, though narrower than its 2022 red ink. Lanxess’s 2023 sales fell 17% from 2022, and by 2024 its EBITDA margin dipped into the high single digits—far from its 2019–20 marks. Although some free cash flow rebounded in 2023–24 as they offloaded expensive inventories and cut discretionary capex, these companies still wrestle with compressed margins, high net debt (Lanxess is hovering above 4× net debt/EBITDA), or forced capacity closures—such as BASF’s permanent downsizing at Ludwigshafen. Meanwhile, more resilient or flexible names—Holcim (SWX:HOLN), Saint-Gobain (EPA:SGO), Wienerberger (VIE:WIE), Yara (OSL:YAR), and Linde (NYSE:LIN)—have, on the whole, kept healthier balance sheets and margin profiles into 2024–25. Holcim’s net income rose further in 2023, aided by relatively contained petcoke and coal costs plus strategic hedges. Saint-Gobain just concluded a year of double-digit operating margins thanks to ongoing energy coverage, a record €48–50 billion in sales, and fresh acquisitions in high-growth insulation lines. Yara, though forced to idle as much as 35% of its European ammonia capacity in 2022, improved 2023 EBITDA to over $2 billion once fertilizer prices moderated but stayed profitable. Linde’s global pass-through contracts and continuing share buybacks underscore how effectively it hedged local volatility. Although all these “hedged” names also endured some 2024 volume weakness, their multi-year swaps, integrated supply, or ability to pass through costs in real time curbed the bulk of the crisis’s impact, leaving them less encumbered by debt or impairments.

That difference underpins a potential paired trade. Going long the battered cluster—ArcelorMittal, Covestro, Lanxess, BASF, and Heidelberg Materials—targets companies still suffering margin pressures or working down high-cost inventory from 2022, yet poised to rebound if EU energy prices keep sliding and volumes normalize further in 2025. If natural gas returns to the teens or low €20s/MWh and lost capacity restarts (Covestro’s core polymer lines, ArcelorMittal’s mothballed blast furnaces, BASF’s scaled-down ammonia plants), these could quickly reprice. Meanwhile, shorting the “energy fortress” group—Holcim, Saint-Gobain, Wienerberger, Yara, and Linde—allows investors to fund those longs in a market-neutral position. The rationale is that, should Europe’s crisis premium fade, the advantage these hedged names enjoyed when gas was 6–10× normal levels will erode. Indeed, recent 2023–24 earnings show how robust hedges or pass-through soared in 2022–23 but began waning once costs and selling prices both eased. By going short these disciplined industrials and long the battered, an investor could ride any upside from an eventual end to the war in Ukraine or a resurgence of Russian gas flows—pushing TTF back down and reversing the cost burdens that hammered unhedged industrials, all while avoiding direct macro bets on the broader European industrial market and it’s cyclical tendencies.

Travel & Tourism: Eagerly Eyeing an Eastern Revival

One of the more dramatic transformations of the war was how quickly airlines had to abandon Ukrainian routes or circumvent Russian airspace. Now, with the occupant of the White House and the Kremlin forging a new “understanding,” carriers like Wizz Air (LON: WIZZ) are salivating at the prospect of reopening 30 or so routes they had in Ukraine pre-war. They’ve publicly stated they could do it within weeks if a stable ceasefire emerges. That’s an immediate tailwind to Wizz’s bottom line, if it materializes.

Ryanair (NASDAQ: RYAAY), the giant low-cost airline, also stands to benefit from any broad rebound in Eastern European travel, though it doesn’t have quite the direct Ukraine exposure that Wizz does. And then we have Finnair (HEL: FIA1S). Before the war, Finnair’s unique selling point was short Asia-Europe travel via Russian airspace over the top of the globe. With that airspace shut, Finnair had to operate lengthy detours, killing its cost advantage.

If these US–Russia talks lead to a partial reopening of Russian skies, Finnair might reclaim that profitable niche. The big question is whether a newly minted peace arrangement includes a side deal on aviation. If the occupant of the White House is serious about normalizing ties with Russia, anything’s possible.

Banks in the Region: War-Sponsor Lists and Cheering Relief

A “peace soon” scenario offers a powerful jolt for banks active in Eastern Europe or saddled with Russian operations. Trump 2.0 seems keen to remove “irritants” like sanctions, which have forced certain lenders to freeze or exit profitable but politically fraught businesses. Austria’s Raiffeisen Bank International (VIE: RBI / OTC: RAIFY) shows how lucrative that can be: it’s the largest Western bank still in Russia—where, by late 2024, nearly 60% of RBI’s revenue originated—and also has a deep footprint in Ukraine. With war raging, this double exposure has been a regulatory headache. But if peace arrives, RBI might recoup value from its Russian unit, plus capture financing opportunities as Ukraine rebuilds. Investors clearly anticipate some upside: the stock soared ~80% in late 2023 on the mere possibility of reconstruction.

Hungary’s OTP Bank (BUD: OTP) finds itself in a similar predicament. It was blacklisted by Kyiv as a “war sponsor” for keeping ties with Russia, though Ukraine has reportedly suspended that label. If Washington or EU donors tie reconstruction funds to removing OTP from blacklists, the bank’s shares might reprice—assuming Zelenskiy, who wasn’t exactly invited to these “peace” talks, goes along.

Italy’s Intesa Sanpaolo (BIT: ISP) also stands to benefit. Though its Ukraine exposure is smaller than Raiffeisen’s, Intesa owns Pravex Bank (45 branches, 780 staff) and continued supporting Ukrainian customers through the conflict. That on-the-ground presence might position Intesa to finance major Italian (and broader EU) contracts in a post-war economy. On the Russian side, Intesa had historically facilitated over half of Russia–Italy commercial transactions, so a deal could restore some lines of business (Italy’s Melony has cozied up to Trump, I expect that will pay off for Italy in an agreement with Russia).

UniCredit (BIT: UCG / OTC: UNCRY) rounds out the cast: it too runs a Russian subsidiary that produced around 8% of group profit as of late 2024—a precarious but potentially valuable asset if sanctions ease. In addition, UniCredit’s broad network in Central Europe means it can help funnel reconstruction dollars or EU-backed guarantees into Ukraine. All these banks, however, must navigate a thicket of political demands. If Zelenskiy or the EU balk at any “peace deal” hammered out without Ukraine’s input, the whole scenario might implode, leaving these stocks languishing. But in the short term, Trump seeking a deal to cement his reputation as the great dealmaker, could lift the clouds hanging over them. War-sponsor labels might be erased, Russian units could be spun off more profitably, and new cross-border loans or donor-backed guarantees might turbocharge the region’s credit growth. In short, a genuine ceasefire—however uneasy—would likely spark relief rallies for these Eastern-exposed lenders.

Defense Stocks: Might the War Premium Dip?

It’s no secret that Europe’s defense spending has skyrocketed in recent years, hitting an eye-watering $345 billion across Central and Western Europe in 2022—eclipsing even the old 1989 peak. Germany alone whipped up a €100 billion war chest, Poland is leading the charge with some 5% of GDP on its military, and Finland’s 36% budget jump in 2022 shows just how alarmed everyone got after Russia marched into Ukraine. All this money doesn’t just vanish into the bureaucratic ether: it flows straight into corporate coffers at the likes of Rheinmetall, BAE Systems, Leonardo, Saab, Thales, and Airbus Defence & Space, turning them into juggernauts with record surges in revenue, free cash flow, and multi-year backlogs. BAE’s top line soared over 20% since 2020 to £23.1 billion, Rheinmetall’s soared 22% to €7.2 billion, and Saab clocked an incredible 46% bump to SEK 51.6 billion, just to name a few headliners. Meanwhile, we’re seeing 11–12% EBIT margins and order books so fat that they’re worth anywhere from two to five times annual sales—Rheinmetall alone has racked up nearly €40 billion in backlog (over five times its 2023 revenue), while BAE is sitting on a comfortable £77 billion pipeline. Factor in the EU’s newfangled R&D grants, cross-border fighter jet collaborations (like FCAS and GCAP), and the not-so-subtle “please build more ammo” requests from multiple ministries, and it’s hard to overstate how golden these days are for Europe’s arms makers.

On top of that, numbers don’t lie: from multi-billion helicopter deals (Leonardo’s AW149 contract in Poland) to full-blown expansions in Sweden (Saab hiring thousands to meet NATO-level production), the new defense mania has catapulted net profits and free cash flows. Companies are reinvesting in capacity—more lines for artillery shells, more workers for next-gen fighter jets—and still rewarding shareholders with dividends and buybacks. Thales’s EBIT cracked €2.1 billion in 2023 on €18.4 billion in sales and an expected 6.5% growth on the year when they report their Q4 2024, BAE’s operating profit rose to £2.57 billion with a robust 11% margin, and Airbus Defence & Space bagged a 15% increase in new orders, crossing €15.7 billion even though it competes with its better-known commercial sibling. Throw in France’s Big Three (Thales, Dassault, MBDA) collectively raking in €27.7 billion in revenue and over €101 billion in backlog, or the unstoppable backlog expansions at Saab, and you get a picture of an industry on multi-year upswing—fueled by NATO expansions, fear of further aggression, and full-blown EU policies that practically beg these firms to keep cranking out tanks and jets.

Yet all that “war premium” could unravel in the short term if a ceasefire is negotiated with Moscow. Markets that have priced in a perpetual arms boom may pivot the moment headlines hint at peace, penalizing stocks like Rheinmetall—up nearly fivefold since 2022 on the back of 12.8% operating margins and €535 million net profit in 2023. A sudden lull in new contracts or a perceived break in hostilities might tempt investors to lock in gains across the Euro military industrial complex at any U.S.-brokered “compromise” that underpinned Europe’s reorder cycle. That’s why I’m eyeing short positions on select defense names—particularly Rheinmetall—via six-month options to catch a knee-jerk sell-off. Be warned, though: multi-year budget laws, 2–5% GDP targets, and unstoppable advanced R&D pipelines mean these companies could roar back once the peace euphoria fades. So the trade is all about timing that initial correction—beyond that, the fundamental drivers of Europe’s defense renaissance still look locked in for years.

Quick Macro Round

Long EUR and GBP: A credible peace deal in Ukraine would remove one of the biggest geopolitical overhangs on the euro, which has traded at a “war discount” ever since energy prices soared and recession fears took hold in Europe. Lower energy costs would immediately help cool Eurozone inflation, giving the ECB scope to slow or pause rate hikes—particularly with nominal German 10-year yields already near their cycle highs around 2.5%. Meanwhile, the euro’s correlation with gas prices suggests a strong bounce if Russian supply fears ease: natural gas could drift back to the low €20-25s per MWh, and that tailwind should quickly flow into the euro’s exchange rate. Sterling (GBP) would similarly stand to benefit, despite the UK’s “twin deficit” vulnerabilities. While gilt yields have climbed partly due to fiscal concerns, a more stable European environment plus reduced global risk aversion could lift the pound off its recent lows—especially if the Bank of England pivots from tightening as economic pressures and inflation expectations recede. In short, both EUR and GBP have room to appreciate when Europe is no longer the epicenter of a high-stakes geopolitical crisis.

Long European Bonds: Beyond currency appreciation, an end to hostilities in Ukraine would likely catalyze a bullish move in European government bonds. Peace lowers tail-risk scenarios, reduces inflationary energy shocks (but let’s remind our selves more in Europe is leaning deflationary), and alleviates some of the market’s term-premium anxiety. From the data, German Bund yields have already priced in a hawkish ECB stance (2y yields near multi-year highs), yet a plunge in gas-driven inflation could shift the monetary policy outlook dovishly. That sets the stage for rallies in both German core duration and peripheral markets like Italy (BTPs), where spreads have widened from 100bp to 120bp, despite Italy’s relatively stable political situation and service-oriented growth resilience. A quick drop in inflation expectations also reduces the risk that central banks will have to maintain restrictive rates for long—traders may even start pricing faster cuts through 2025. Taken together, the combination of receeding energy inflation coupled with lagging growth (although cheaper energy should be a boost to growth, but European fiscal drama likely outweighs this benefit), receding geopolitical tensions underpins a near-term bullish case for European bonds, making long positions (especially in the 2-year segment) an appealing risk-reward proposition over the next 6 months.

Short Taiwanese Semi’s: less obvious but depending on the type of agreement struck, it could embolden further Chinese aggressions on Taiwan; specifically semi’s given they are their most high value add and high multiple industry which also works as a hedge for both our U.S. tech exposure and our Chinese tech exposure simultaneously. (More on this when I cover Chinese equities, we have been long BABA with calls as mentioned in the Chat and broad Chinese Tech Equities)

Long Gold, plenty of reasons we have gone into to own Gold and we remain gold in case no deal comes up. Do not expect a deal on Ukraine falling through would materially impact the price though positively and if a deal comes up, I’ll own more long term OTM calls. (this has been a 5% of NAV in 1+ year option premium position and will maintain it as long as the curve is structurally steepening.)

You could also short some energy companies that benefited from the windfall of war though higher energy prices and remapping energy flows, my views here remain bullish for these equities given our last article on European energy issues, so I am not putting a short on these. Remaining long is also a hedge to a no-deal scenario.

Infrastructure and Construction: The Next Marshall Plan

Ukraine’s reconstruction needs now hover around $486 billion—far exceeding the country’s economic capacity given that its GDP is only forecast to reach about $183.59 billion by the end of 2025. In the immediate term, efforts focus on repairing damage in safer areas—restoring basic services, clearing debris, fixing housing that absorbed $80 billion of losses, and stabilizing core infrastructure amid periodic attacks on power grids and transport routes. Medium-term plans revolve around ramping up large-scale projects for roads, railways, bridges, and utilities, with a blend of donor funding (G7, IMF, World Bank) and private capital drawn by new war-risk insurance frameworks and a proposed “reconstruction bank” designed in partnership with BlackRock and JPMorgan. These measures aim to close persistent funding gaps and reduce corruption risks (good luck with that), allowing broader rebuilding even while the conflict remains unresolved in some regions. Execution still faces steep hurdles—demining vast areas, procuring building materials in quantities rarely seen on a single front, and mobilizing both a depleted domestic workforce and international firms brave enough to operate in a high-risk environment.

From an investor’s perspective, a set of publicly traded names stands out. Heavy-machinery leaders like Caterpillar (NYSE: CAT) and Volvo Group (STO: VOLV-B) appear poised to supply bulldozers, excavators, and trucks needed to reconstruct highways, clear rubble, and restore farming infrastructure. Building-materials giants CRH (NYSE: CRH) and Holcim (SWX: HOLN) should see soaring cement demand; CRH has already expanded its Ukrainian cement capacity. ArcelorMittal (NYSE: MT) can ramp up steel output at its Kryvyi Rih plant for rebar and beams once large-scale housing and industrial projects come online. Engineering and consulting specialists such as AECOM (NYSE: ACM) and Jacobs Solutions (NYSE: J) can secure project-management roles, while Schneider Electric (EPA: SU) and Siemens (ETR: SIE) will likely modernize outdated/damaged electrical systems. In logistics, Maersk (CPH: MAERSK-B) and Deutsche Post DHL (ETR: DPW) are well-positioned to handle the flood of raw materials across Poland and Romania, and energy companies like RWE (ETR: RWE) or Ørsted (CPH: ORSTED) could benefit if Ukraine’s future power grid relies more on renewables and decentralized technology. Although war-time conditions persist, the scale of the rebuild—essentially Europe’s largest in generations—suggests these firms may tap a substantial revenue stream once the bulk of donor money and private investment starts flowing into major contracts.

I have no trade here but an idea that some could enjoy the risk/reward of, I don’t think this can be appropriately expressed with options. Spot only strategy would work best. I would likely wait for real progress to be made and move the 2.5% to this bucket for longer term investment. Not all the companies mentioned above would make for good trades btw. Just initial ideas while we wait and see how things take shape.

Our Espressos are Stone Cold by Now

So yes, mon ami, our espressos are stone-cold and the Trump team is off forging a “peace” that forgets to invite the side still under attack—yet from a purely mercenary vantage, the whiff of a ceasefire might whip markets into a frenzy, sending battered industrials, airlines, and Eastern European banks soaring just as defense darlings and scarcity-chasing energy firms deflate like an old soufflé. Of course, if Zelenskiy denounces this diplomatic theater or Europe breaks out in a moral rash at letting Russia claim any gains, we’ll pivot right back to risk-off—and the Trump may refocus to a new spectacle altogether. But for the moment, it seems likely that capital will allocate to the range of “peace trades,” buoyed by the idea that cheap gas and open air routes are a necessary part of a European deal (keeping in mind American energy has strongly benefited from this war with increased costly LNG exports to the EU). At it’s core, this situation is darkly comedic: Trump once scorned for ignoring alliances is now waltzing with Russia, leaving Ukraine on the sidelines and Europe grumbling in the background. Meanwhile, I’ll keep swirling my Bordeaux, half-expecting the White House to auto-declare a Nobel Prize, while the EU scrambles to remember its strategic autonomy. Still, c’est la vie; keep your cynicism and your trading discipline tight—because if this deal-in-name-only gains traction, markets could indulge in a giddy rally before confronting geopolitical realities. Bon courage.

Cheers!