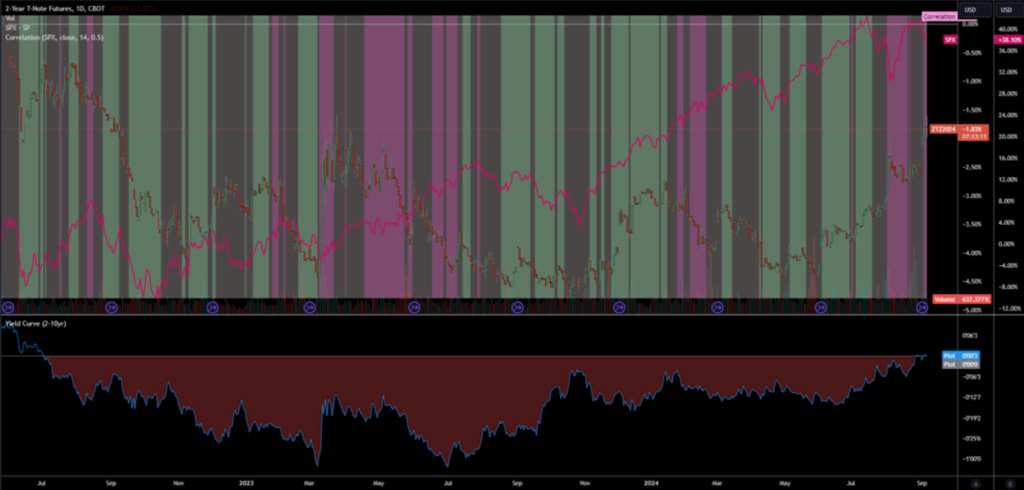

STIR butterflies from Yield curve flip flops

How should we think of our rates hedges to lazy equity longs now?

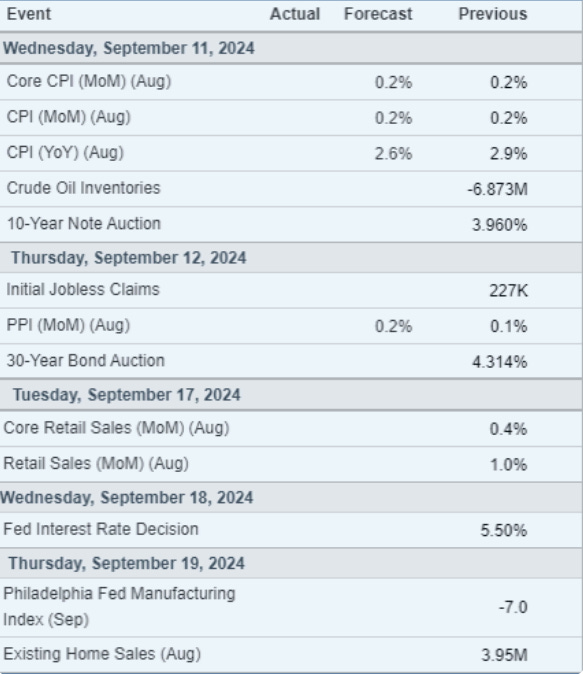

This early September 2024, we commemorate the un-inversion of the yield curve (looking at 2s10s), which first inverted on July 7th, 2022. This repricing of rates across developed economies came in after Friday’s so-so job numbers, which failed to confirm the growth scare narrative but did confirm a slowing of growth consistent with the normalization of the economy from tapering inflation in the shorter term. The economic print allows us to verify that there is a palpable reduction in employment options, and new jobs are coming in at a slower pace. Tomorrow’s inflation numbers will help establish the probability that disinflation evolves into deflation and, by extension, possibly into a contraction in growth and rapid acceleration of unemployment. In the long term, I expect inflation will retake center stage. This is due to pro-labor policies taking hold globally, which translates into government-led spending and policies to support wage and employment growth, including defending the currency from devaluation by the central bank (future note on this topic but mexico is a great example of this trend). There will likely be little room for a deep recession as policy-led spending will put a floor on the weakening of growth in exchange for inflation. Although this is a shift we can start building a hedge for, it takes second place to the more immediate repricing of assets from growth projections.

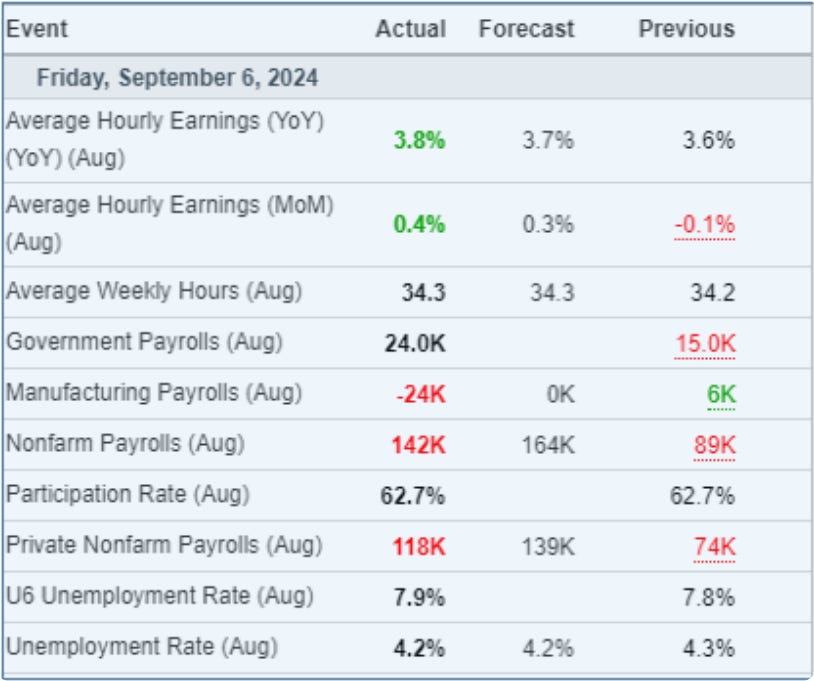

Looking at the mixed signals from Friday Sept 6’th, employment figures:

This print indicated that overall employment continues to support economic growth at a slower pace, in line with the framework laid out in this note:

What is my credit card limit?

How has Yellen’s shopping been doing?

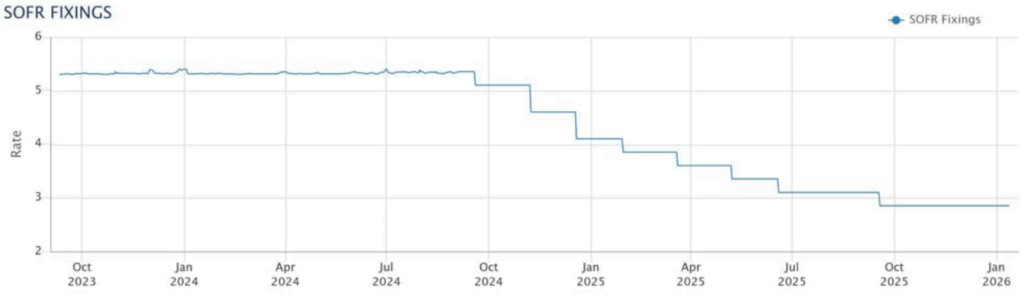

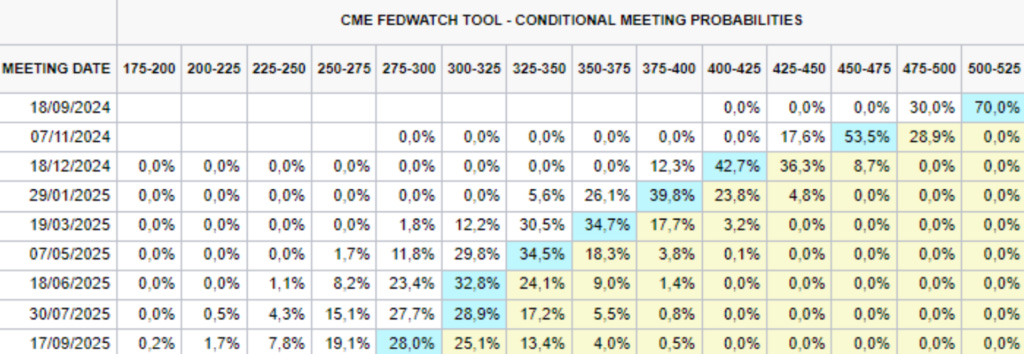

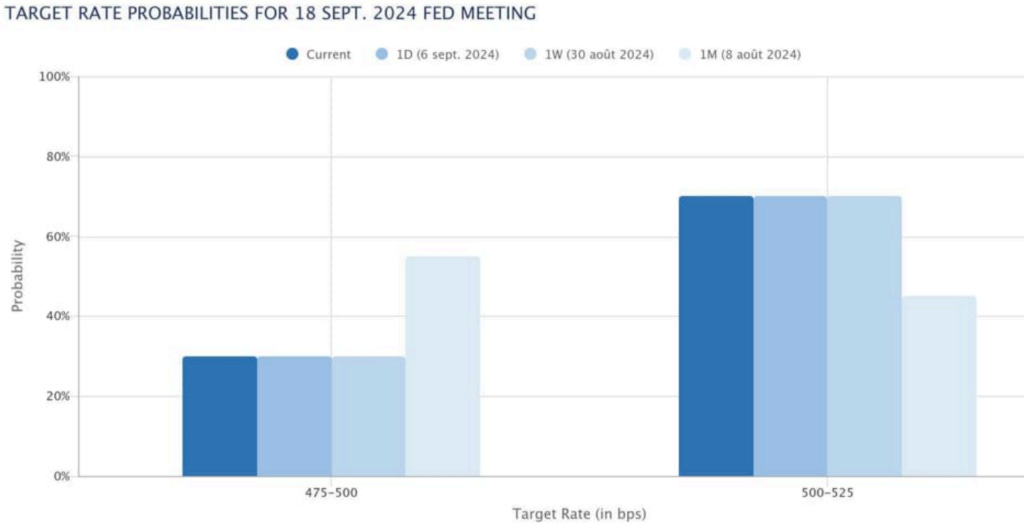

The market broadly interpreted the data to imply a 25bps cut (70% chance) over 50bps at the next Fed policy meeting. Here are some charts that provide context as to the market reaction:

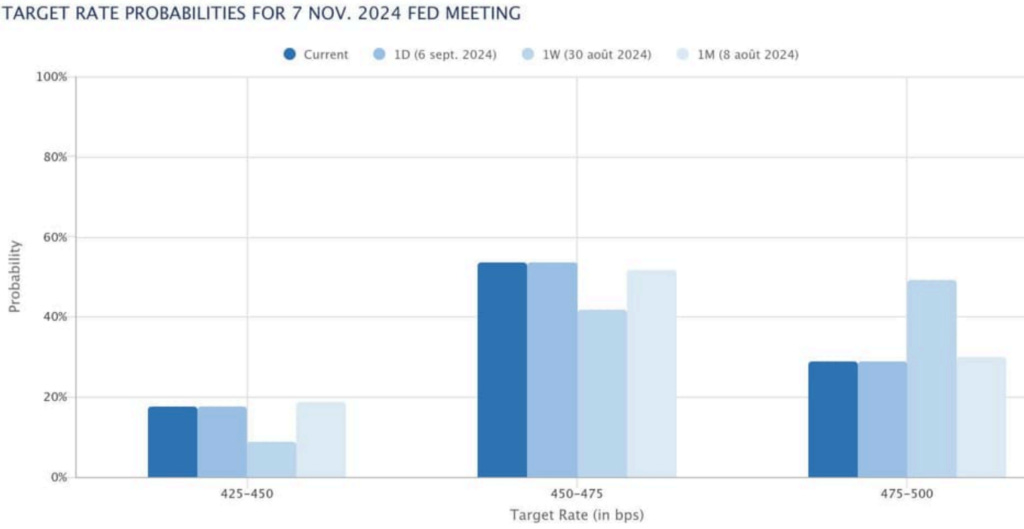

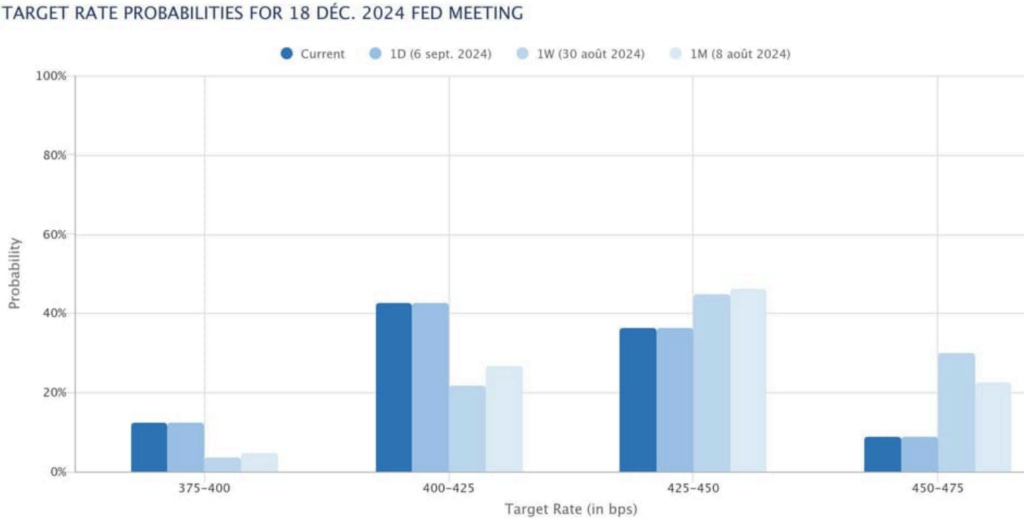

We note here the impact on the Nov 7 meeting pricing from the jobs print, which increased the market-implied likelihood of an additional 25bps or 50bps cut vs no additional cuts. This shows that the jobs report, while quite mixed, was viewed by the market as skewed to the downside, hence the pricing for the subsequent meeting. A similar story can be read in the December meeting as well.

The policy rate could be reduced by 25bps for the following reasons:

The Fed is biased not to be seen as political and provide economic stimulus potentially benefiting the election results in favor of the sitting administration. This would bar a reduction of the policy rate beyond what the economic data implies as being the minimal necessary cut.

The Fed does not like being wrong, and a 50bps cut would imply it has been overly patient when warning signs of growth slowing had already appeared before the last meeting.

The Fed will likely offer up a reverse Greenspan (dotcom crisis) and issue successive 25bps cuts up to the point that it considers supportive of the labor market while not stimulating inflation excessively as a simple solution to the tensions in the labor market.

The jobs market has proven to be resilient thus far and consumer spending is healthy despite tight monetary conditions (but not that tight as explained in the reverse repo note), and the weakening was to be expected from a normalization of inflation.

A Reverse Repo Story

Show me the Money!

And could be cut by 50bps for the following reasons:

A 25bps cut would not stimulate the economy in the short run ahead of the next meeting but only provide the stepping stone to future stimulus. This is due to current contract pricing in the possibility of 50bps at 30%, so a 25bps cut would effectively tighten financial conditions on the short end of the curve. Moreover, a 25bps cut would do little to reprice rates on the long end where corporates borrow and would see improvements on their balance sheets that can eventually translate into more job creation and improved wages. The Fed would need to be deeply convinced that the labor market is on the verge of a steep deterioration before taking the 50bps route, but why not just 75 or 100bps in that case?

In aggregate, 25bps is the path of least resistance. There is, however, little asymmetry in taking that view. Even betting on a 50bps cut provides a poor risk-reward (2 to 1 on STIR future options) if it is eventually justified. It would be more interesting to look at the total number of cuts in a longer timeframe to put on a hedge with more convexity (in the risk-reward sense, not bond math).

This week’s inflation numbers will be used to gauge the rate of change in growth slowing, and I suspect a slightly hotter inflation print would be welcome by equities.

If the CPI numbers and subsequent initial jobless claims come in cooler and weak, respectively, that could increase the market-implied probability of a 50bps cut, and there might be something to do here on the short end, but patience for now.

The bull-steepner has been one of the trades mentioned in the following publication:

The tale of Goldilocks being eaten by the Bears

I have been to many stakings- you have to know where to stand! You know, everything in life is positioning, positioning, positioning…

It was put on as a hedge to equities moving sideways or down and has been an excellent way to smoothen out the returns on a lazy-equity long book through the rotations in equity-bond correlations, namely on Aug 5’th where it had managed to provide a quarter’s worth of hedge PnL and was promptly taken off.

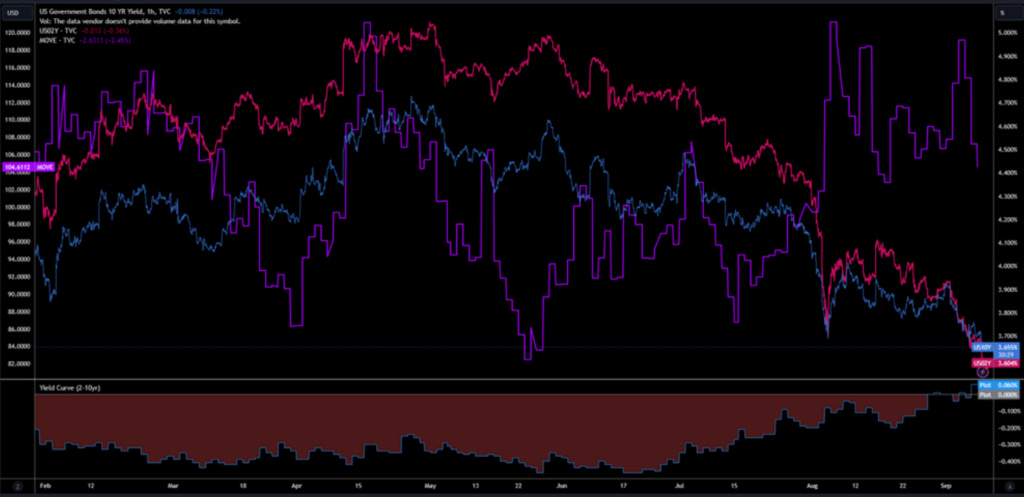

Now that the curve has steepened to the point of being flat, we should consider if there are better opportunities in the rates complex to position hedges and if the bull-steepner could still provide opportunities despite being crowded.

On a practical note, what does flattening mean when determining the flow of capital? Simply put, that risk can move to longer durations by having yields now equivalent to the short end and credit spreads not widening despite growth scares. This implies there will be a natural bid from safe-yield seeking institutions moving towards further durations, solidifying this uninversion; this means that we now have a natural floor for yields on 10’s relative to 2’s. We are unlikely to see the curve invert again, given the Fed’s cutting path, which is now well-telegraphed. I mention credit spreads in the above relation as default probabilities evolve at a multiplicative rate at longer timeframes.

Making a quick parenthesis away from rates, I find it somewhat perplexing that credit spreads have not widened through August and have persisted their downward, starting in Q3 of 2022.

Now, my confusion can be explained away by noting that corporations have navigated the earnings season without showing signs of worsening balance sheets and continue on a path of earnings growth, albeit with some notable expectation management from executives.

I am not willing to bet that credit spreads will widen substantially anytime soon, and hope to make money on it. However, I would want to buy meltdown insurance for as little carry as possible, given the tensions in the broad market with CDS spreads being relatively tight (CDS spreads should remain at these levels given my base case as outlined in the consumer outlook piece linked above, but I like to suffer less when I am wrong).

The HYG/HYGH etf (High Yield Bonds and its rates hedged brother) is intuitively the most straightforward way to do this, and a well-timed short would have paid during Aug 5’th (I don’t like any strategy that requires good timing…).

Well-timed is key for the HYG complex, given bid/ask on options wipe out half the value if you were to regret placing the trade on the same day, and borrowing a unit to go short means you need to pay up the 8.79% dividend yield in addition to your brokers stock borrow costs. This gets quite expensive quite quickly.

One other option is using inverse etf’s like SJB. Like most inverse etf’s these track daily performance, which for highly volatile underlying erodes value very quickly (they will end up buying high and selling low by construction on volatility spikes). The saving grace here is two-fold. First, the instrument pays you a respectable 5.07% div yield from the underlying treasuries used as collateral for the default swaps held in the trust. Second, volatility is generally subdued and constant in the high-yield bond index due to credit spreads being compressed and increases in volatility have come from negative credit views supporting the value of SJB relative to its benchmark irrespective of when you put on the trade relative to a traditional short with no daily hedging. This means it has tracked well the inverse index with minimal erosion and would provide protection when vol spikes during a negative credit event. Given I don’t think there is room for CDS spreads to move lower from here, there is some convexity to be had from this instrument in terms of payoff for protection against a deterioration of credit conditions.

For now, I would have this instrument at some 50bps of NAV and stick to the primary hedging strategy of straddles maximizing for gamma that benefit from dispersion widening (following note) until I find a cleaner pure play on widening credit spreads suitable for retail (and taking any insight to be had on this topic!).

Back to rates and our lazy equity-long rates hedging problem…

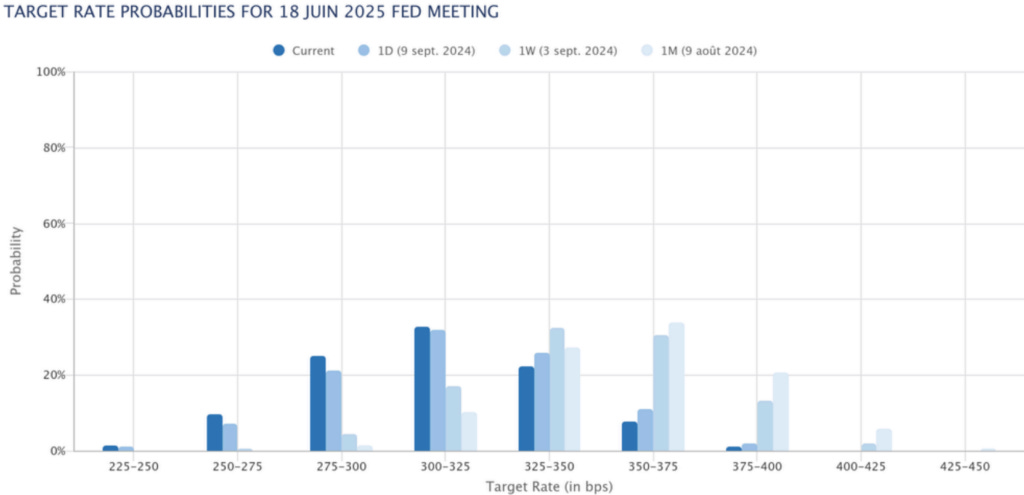

Currently, the rates market is implying a 50/50 chance of hard landing when interpreting that as the distribution of bets on the June FOMC meeting will bring the benchmark below a 3% level. Here is the distribution change for the June meeting:

The reader can quickly derive this probability on a spreadsheet pricing butterflies on June STIR contracts where the ratio of the cost vs the payoff is a simple proxy to likelihood. For context, if the Fed cuts by 25bps every meeting to June, the rate should be in the 3.75% range, so the market implies an additional 75bps of cuts to our base case between now and June’s meeting.

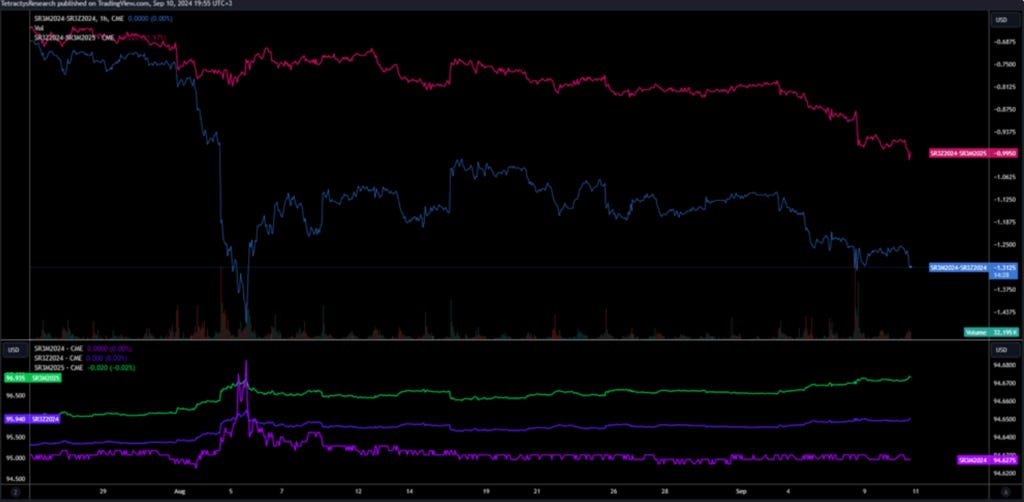

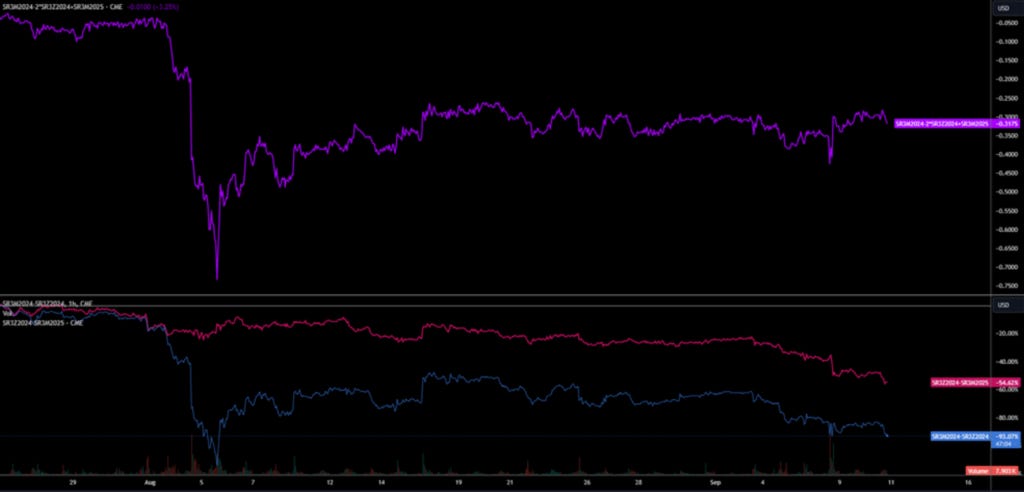

Given the mixed to positive economic data (but inflation TBD) and current path by the Fed through the end of the year being reasonably well-telegraphed, I would be long SRM4Z4 (steepner, long and short respectively the M4 and Z4) taking into account concerns that the economy could deteriorate. The Fed be forced at a later stage to cut deeper than current expectations on the back of negative news, I would short SRZ4M5 (flatner, short and long respectively the Z4 and M5) providing us with an elegant hedging solution given rich pricing saying to the market: you are wrong in the short run, Powel won’t frontload cuts anywhere close to the election and data prior the end of year will show the economy is still growing in line with its reduction of inflation, but maybe you are not wrong in the longer term, and there could be a recession, so I’ll tag along with that as a hedge. This is the plot of the SRM4Z4M5 butterfly where we sell the belly (1/-2/1) of the curve:

I’ll start unwinding the steepner if economic data starts coming in negatively earlier than the mixed signals I expect for the next few months in line with the note on consumers and move that capital to the flatner portion of the trade.

If economic data starts improving on both the growth front and inflation, the flatner portion of the trade can be changed to steepner to go in line with the 25bps successive cuts view we laid out. The downside is that it would lose its hedging value for unforeseen downside shocks to the economy.

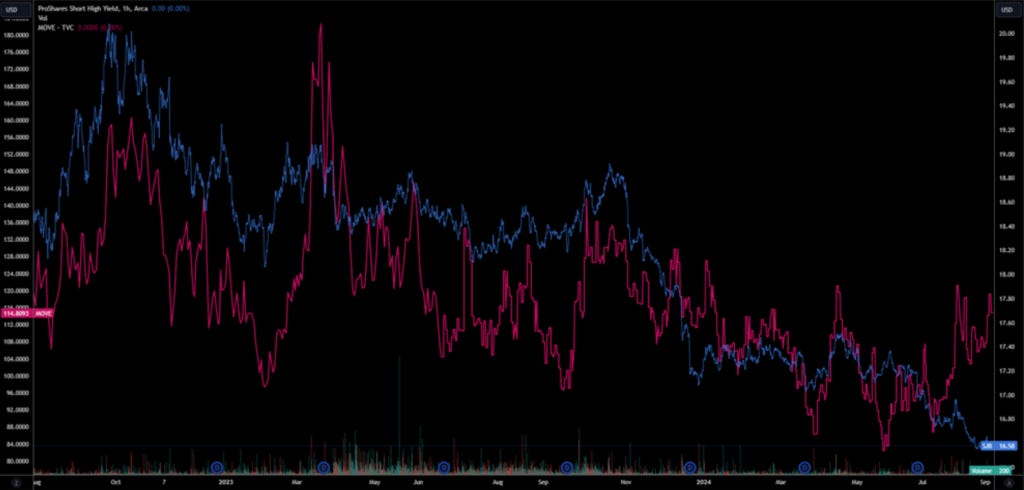

Now we need to go back to evaluating the bull-steepner on the yield curve, which we took off on Aug 5’th. We remain at a point of heightened bond volatility, as seen through the MOVE index.

Relatively high bond vol in conjunction with the current consensus pricing of the steepner trade on 2s10s and pessimistic view on the economy makes this position broadly unattractive to put on. The primary two arguments I see to put back on the long on 2s10s is that now that the curve has uninverted, there will be a natural shift of capital towards the long end, putting a natural bid on it and providing us with a limited downside to the position barring any change in Fed cutting trajectory. Moreover, this trade, although already richly priced given the recessionary view that bonds are showing, offers a good hedge for worse-than-expected economic prints where this position could see another Aug 5th style of risk aversion pricing, which is where this trade shines.

I would consider adding position back tactically on any pullbacks on the spread. I expect that FOMC will be the correct opportunity to go long bonds via ZT and ZN after the expectations on the 50bps cut get washed away, and we see pricing along the curve fall in line with 25bps each meeting, assuming that the data keeps coming in mixed.

From a portfolio construction perspective, this is now a good time to be cyclically long equities and bonds. There are two main scenarios for financial markets:

1) Economic prints keep coming in mixed to good and we continue a goldilocks regime where equities are skewed to the upside while bonds yields drop (70% chance)

2) Economic prints come in mixed to bad and the bears eat goldilocks where bonds should be in a sustained bull market while equities get repriced downwards (30%)

Cheers!